Quarterly Summary

Brent crude oil prices fluctuated throughout 2024, peaking at US$93/bbl in April before declining towards the end of the year. The 4Q average stood at US$74.6/bbl, down from US$80/bbl in 3Q and an average of US$82.6/bbl from the preceding quarters. A 2% year-on-year decline in China’s crude imports—its first annual drop in three years—contributed to weaker demand, prompting OPEC+ to delay the unwinding of 2.2 mmbpd in voluntary production cuts to April 2025 and extending these measures through December 2026. As a result of continued OPEC+ production restrictions, Saudi Aramco reportedly sent rig suspension notices to contractors for around 50 land rigs in Saudi Arabia during 2H 2024. These rigs, all of which were focused on oil drilling, have been suspended for a period of up to 12 months.

Increased supply from non-OPEC countries, such as Brazil, Guyana, and the United States, continued to influence Brent pricing dynamics and put pressure on the effectiveness of OPEC+ production cuts. The US crude output peaked at 13.6 mmbpd during 4Q 2024, while NGL production grew to an estimated 7.4 mmbpd, up 3% and 8.8% on 2023, respectively. Growth in US output could continue beyond 2024, supported by a shift in government policies and sentiments, as seen in the Trump administration. However, oil and gas prices will likely remain the main driver of drilling activity in the US, with operators focusing on profits over sheer production growth.

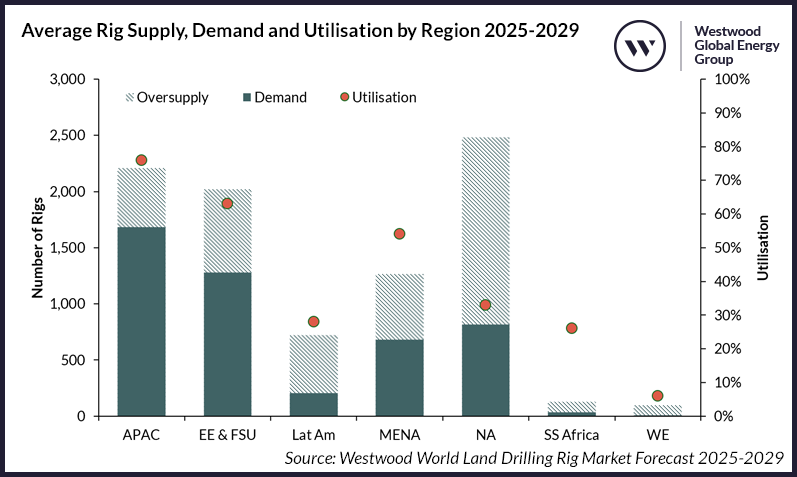

Despite concerns over demand growth and the suspensions in Saudi Arabia, 4Q 2024 closed out a broadly positive year for land rig activity. The recently published World Land Drilling Rig Market Forecast, which offers an in-depth outlook for the land drilling rig market from 2025 to 2029, indicated that global rig demand averaged 4,489 in 2024, a 1% rise on 2023, but a decline was recorded in several markets, including Eastern Europe, Saudi Arabia and the USA, counterbalanced by growth in the APAC region.

Westwood forecasts a decline in global rig demand in 2025, falling from 4,489 rigs in 2024 to 4,413 rigs. However, demand is expected to rebound in 2026, driven by demand from Asia-Pacific and MENA. Supply over 2025-2029 is expected to average 8,928 drilling capable rigs, with global rig utilisation of 50%, in 2025 increasing to 54% in 2027, and remaining stable through 2029.

Average Rig Supply, Demand and Utilisation by Region 2025-2029

Source: Westwood World Land Drilling Rig Market Forecast

Nabors’ acquisition of Parker Wellbore for US$472 million (mn), taking on Parker Wellbore’s 17 rigs located across the USA, Mexico, Kazakhstan, and Bangladesh. Notable field acquisitions occurred in Canada, where Chevron Canada announced the sale of its 20% non-operated interest in the Athabasca Oil Sands Project and 70% operated interest in the Duvernay shale to Canadian Natural Resources Limited for US$6.5 billion (bn), while Ovintiv acquired Paramount Resources’ 109,000 net acres in Montney for US$2.377bn. It was also a busy quarter for geothermal activity, with Australia and Indonesia both announcing exploration rounds, while approvals for projects were recorded in Germany and Iceland, among others.

Ben Wilby

Senior Analyst, Onshore Energy Services

[email protected]

Deborah Yamba

Research Analyst, Onshore Energy Services

[email protected]