Quarterly Summary

Concerns over global demand dominated the oil markets in 3Q 2024, with Brent crude prices falling from an average of US$85/bbl in 2Q to US$80/bbl, despite OPEC+ postponing its unwinding of the 2.2mmbpd of voluntary cuts from September 2024 to run through December 2024. Several data points out of China indicate that lagging demand has driven this, despite 3Q 2024 demand data remaining relatively robust elsewhere. These indicators of slowing demand outweighed short-term uncertainties posed by the escalating tensions between Israel and Iran in the Middle East.

Merger and acquisition (M&A) activity remained robust during the quarter under review, with the headline deal for land rigs being H&P’s US$2bn acquisition of KCA Deutag. Also notable this quarter were the exploration licensing awards for onshore Ghana and Ivory Coast – both countries with little to no recent onshore exploration.

The geothermal sector also saw significant activity in several regions in 3Q 2024. Drilling at the Banska PGP-4 Geothermal Well in Poland resumed after a two-month hiatus caused by a slow rate of drilling and wellbore collapse. Following wellbore cementing, further drilling commenced with a new drill and modified drilling mud. Similarly, in India, the Oil and Natural Gas Corporation (ONGC) restarted drilling at the Puga Valley geothermal project after upgrading equipment and contracting an unidentified rig from Seros Drilling. This quarter also saw tender launches for geothermal exploration and drilling in Indonesia and Nicaragua.

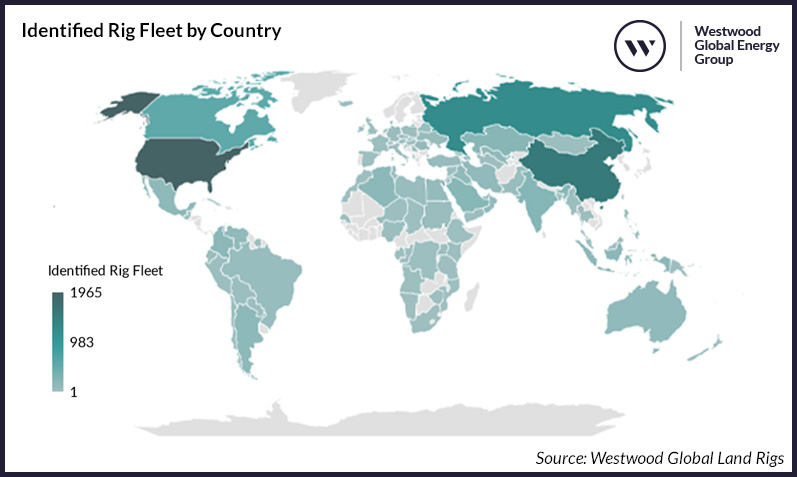

Identified Rig Fleet by Country

Source: Westwood Global Land Rigs

Westwood’s identified rig fleet currently stands at 8,542 rigs globally, led by North America (29% of total), Asia (23%) and EE & FSU (21%). The HP range of the global rig fleet is split relatively evenly between 0-1499 HP (51%) and high HP (49%) – figures that are expected to begin to change in favour of the higher HP units in the coming years. Westwood’s upcoming World Land Drilling Rig Market Forecast 2025-2029 will examine the outlook for demand of both categories on a global scale, highlighting the markets that are increasingly favouring high-HP units, as well as those where the viability of low HP units remain strong.

Ben Wilby

Senior Analyst, Onshore Energy Services

[email protected]

Deborah Yamba

Research Analyst, Onshore Energy Services

[email protected]