FPS Activity Recovery Continues Despite Cautious Investment Climate

The Q3 edition of Westwood Energy’s World Floating Production Systems Tracker, has been released. Across 2018 we have seen the FPS market continue along the path of recovery that began last year. It is evident that the downturn has changed the behaviour of E&P companies when sanctioning FPS projects, and the intense pressure on the supply chain witnessed during the 2015-2017 downturn remains, despite the improvement in oil prices. There has been a much greater focus on the re-engineering of projects to achieve maximum cost efficiency. This capital discipline is the primary reason so many projects continue to see revised timelines. In Q2 2018 we have seen three FPS units ordered. However, in the same quarter, six units that were expected to be ordered this year have been delayed to 2019.

The underlying macro-economic environment is positive, however, with oil prices at levels that support positive free-cash flow for E&P companies and allow investment in new developments. Pricing in offshore OFS markets remain at cycle-lows, compared to onshore markets that are further into a recovery cycle and are seeing price inflation. We are tracking a large number of projects on the ‘starting blocks’ and moving toward sanction that will drive high levels of new orders in the coming 18 months. In total, we expect 65 units to be installed between 2018 and 2022 with a value of $59bn. Orders worth $62bn are also expected over the same period.

The companies that have been successful in the new environment have been those that have adapted to the conditions around them. An example is SBM Offshore whose Fast4Ward hull approach has already resulted in an order for the Liza field in Guyana. BW Offshore’s move to acquire an operating stake in upstream assets has also been positive, allowing them to deploy an off-hire FPSO (the BW Adolo) on a field that they now operate.

Led by Brazil, it is the Americas that drive activity over the forecast. Latin America will lead expenditure for both installations and orders over the forecast, driven by Petrobras in Brazil and Exxon’s continued investment in the Starborek block offshore Guyana. After a period of inactivity, investment will return in deepwater Gulf of Mexico, with a number of FPSS units expected to be ordered over the forecast. Total installation spend of $9bn is expected in the GoM, the highest after Latin America.

This quarter Westwood have added new features into the report including further analysis of upcoming orders and installations, a summary of the key details of the last 12 months in the FPS industry and analysis of the units that are expected to be ordered or become operational over the next 12 months.

Key Conclusions:

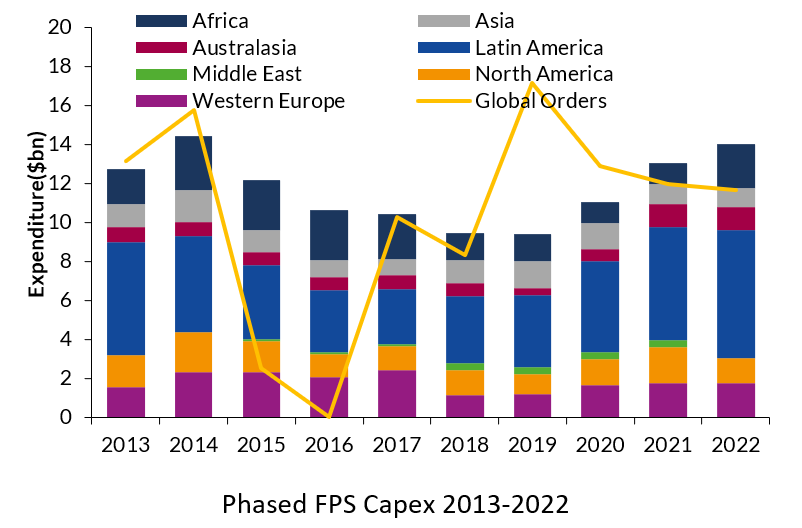

- $62bn worth of orders expected over the 2018-2022 period, $17bn of this to come in 2019.

- Phased development Capex of $57bn forecast for the next five years.

- Backlogs are reaching cyclical lows, however consistent levels of orders will boost expenditure and activity into the 2020’s.

- With spend of $24bn, it is Latin America that accounts for the largest proportion (43%) of phased Capex. This is driven by Petrobras and activity at the Liza field offshore Guyana.

- North American spend will be a key contributor to overall expenditure, accounting for the second largest amount of both expenditure and units.

FPS Market Coverage:

- Installation Capex forecast by region and type.

- Unit installation forecast by region and type.

- Order Capex forecast.

- Analysis of FPSO leasing market.

- Summary of new and expected 2018 orders and units onstream.

- Comparison between reports – highlighting major news stories of the quarter.

Analysis is based on Westwood’s Sectors FPS database, which details more than 700 FPS projects that are updated and tracked daily. The World Floating Production Systems Tracker is essential for anyone evaluating investment opportunities in the FPS sector, including growing firms seeking competitive advantage across segments, investment banks and advisory firms wanting to improve their understanding of the business, and industry analysts seeking a competitive edge.

If you are evaluating current or future investment opportunities in the FPS sector and need to understand the future spend outlook or a unit-by-unit specification assessment, please contact Gareth Hector or a member of the OFS Research team on:

Direct: +44 1795 594 726

Email: [email protected]

Or, complete the form below, and we will be in contact.