A Second Wave – $53 billion of FLNG Investment Expected as Market Bursts Back to Life

Based on Westwood’s latest analysis of sanctioned and upcoming projects, global FLNG capital expenditure (Capex) is projected to total $52.8 billion (bn) over the 2019-2024 period.

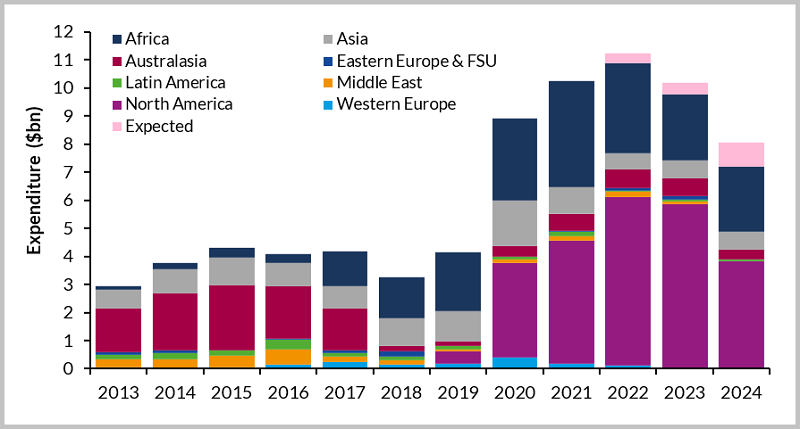

As LNG exports take a foothold in the US, investment in floating liquefaction facilities in North America will play a pivotal role in global FLNG expenditure over the forecast, accounting for 45% of expenditure. A combination of drivers, including perceived technological maturity, an improved macroeconomic outlook, and cost reduction in the supply chain, will support an increase in project sanctioning over the next 24 months.

Following a 22-month hiatus in project sanctioning, the FLNG industry is moving into a ‘second wave’ of developments, with the market opening up to a greater number of participants. The size and technical complexity/risk of early pioneer developments allowed only the largest NOCs and IOCs to move forward with projects on a balance-sheet financing basis. As more FLNG units become operational, we are seeing project structures and financing more akin to the well-established FPSO sector. This includes a move to syndicated project financing (e.g. as arranged for ENI’s Coral South Unit) and Construction Financing / Sale and Leaseback structures (such as Golar’s Hilli Episeyo unit.)

Increased gas demand driven by economic growth and fuel switching combined with ongoing concerns over energy security underpins the import vessels market. The key driver for the use of floating units remains the short lead-time from sanction to operation and consequently, tendering activity for FSRUs is expected to remain strong over the 2019-2024 period.

Global Expenditure on FLNG Facilities by Region, 2013-2024

Contact us to access the latest FLNG project details and forecast databook via SECTORS.

Key Conclusions

- Over the 2019-2024 period, liquefaction vessels will account for 80% forecast expenditure, totalling $42bn. This investment will subsequently lead to the installation 15 FLNG vessels and an addition of 47.9 mmtpa to global export capacity by the end of the forecast period.

- With the challenging market conditions seen over 2015-2017 starting to ease, forecast FLNG expenditure is expected to grow at a 14% CAGR, as operators seek to take advantage of the current competitive pricing structure within the oilfield services and equipment sectors.

- Forecast liquefaction spend in Africa will total $15.4bn over 2019-2024, with 34% of this spend already committed.

- Gas-to-power projects will account for a significant proportion of import vessel demand in Africa and Asia.

- Strong global fundamentals for regasification vessels have prompted some leasing contractors to sign letters of intent (LOI) for optional units to be delivered in the latter years of the forecast.

- A total of 18 countries are expected to have their first floating import vessels installed over the forecast period.

The World FLNG Market Forecast 2019-2024 is presented using Westwood’s SECTORS data with detailed analysis and commentary on eight distinct regions with a twelve-year market view – historic data covering the period 2013-2018 and forecast data for 2019-2024.

Westwood’s SECTORS online data platform identifies project-by-project information, development timeline, and Capex details for both liquefaction and regasification vessels by service type. The report further provides detailed insight on:

- Market drivers and trends.

- FLNG supply chain and contractors.

- FLNG Import and Export expenditure by component and service type.

- Regional expenditure analysis.

- Detailed project appendix for the 2019-2024 period.