OPEC’s aim for market stability further from reality than ever

In Q2 2019, OPEC yet again moved to restrict supply, extending production quotas until at least March 2020. Most recently, comments from OPEC’s Secretary-General Mohammed Barkindo, suggest that cuts could remain in place longer in order to support oil prices. These moves from OPEC highlight the cartel’s desire for both stability in the market and higher oil prices. However, the third quarter has seen anything but stability, with a drone attack on Saudi oil facilities at Abqaiq and Khurais resulting in 1.2 mmbbl/d of lost crude oil for the Kingdom in September. Brent futures saw the biggest one-day percentage gain on record following this but fell less than a week later as Saudi worked to restore the facilities. Outside of this one event however, the key characteristic of oil price has been one of paralysis, with continued strong output from the US, as well as lower demand counteracting the efforts of OPEC and leaving oil price stuck in the high $50 to low $60 range.

Key Conclusions Include:

- OPEC continues to restrict production to stabilise the market, but efforts are expected to be undercut by low demand.

- Global drilling activity will experience considerable growth, with over 424,756 onshore and 12,936 offshore development wells estimated to be drilled over the forecast period.

- Deepwater activity remains a bright spot over the forecast, with production growing 38% from 2019 to 2025. More than 1,315 wells will be drilled to achieve this.

- New plays in East Africa, the Mediterranean and Guyana will help to diversify supply sources.

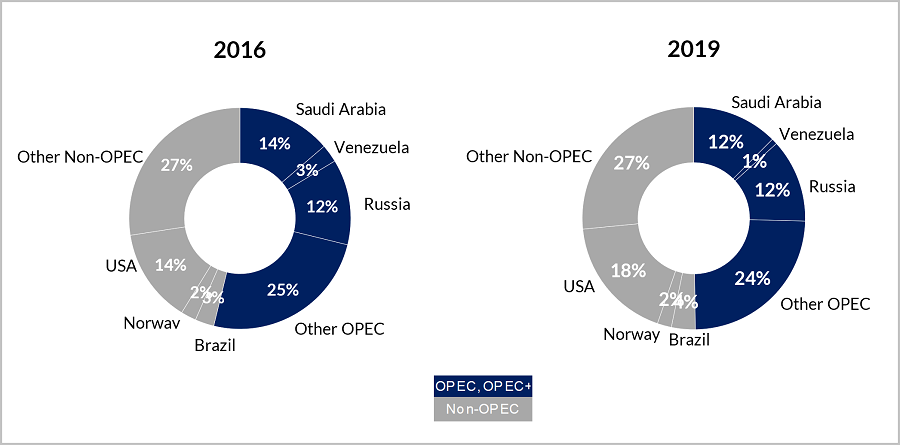

- OPEC cuts and supply additions from outside of the group have changed the balance of global liquids supply.

- OPEC’s cuts have seen its share of global liquids production fall from 54% in 2016, to 50% in 2019.

OPEC and non-OPEC share of global liquids production, 2016 vs 2019

A key story of 2019 has been oil demand. Several forecasters have lowered their demand growth expectations due to a slowdown in the global economy, driven largely by the ongoing US-China trade war, other protectionist policy making and global economic uncertainty. OPEC’s decision to continue production cuts into March 2020, as well as ongoing tensions in Iran, should have tempered supply gains from the US in the short term, however, the weaker demand outlook has led to a continuation of subdued oil prices.

On the supply side, the forecast looks set to see a surge of production. OPEC are not expected to maintain production cuts throughout the whole forecast, and once these end, Middle Eastern output will grow significantly. Westwood expects liquids production to reach 33.2 mmbbl/d in 2025, as Saudi Arabia, Iraq and the UAE invest heavily into brownfield developments. At the same time, significant investment into natural gas projects in the region, including in Qatar, Saudi Arabia and UAE, will lead to an estimated 10% growth in regional gas production in 2025 versus 2019.

In China, Asia’s largest producer, a 78% increase in onshore development drilling activity offers potential to finally achieve a level of production growth from the country’s unconventional reserves, potentially offsetting declining production from mature conventional fields.

Bright spots are appearing in areas with little or no historical production. East Africa and the Mediterranean are both expected to gain market share. In the Mediterranean, the discoveries of Zohr (Egypt), Aphrodite (Cyprus) and Leviathan (Israel) have demonstrated the potential of the area as a new gas producing hotspot.

The vast majority of liquid production will come from countries with a well-established production history, but Guyana continues to exhibit strong growth potential. Following the Liza discovery on the Starbroek block, operator ExxonMobil has made 13 further discoveries. Tullow Oil have also made two discoveries on a different block, indicating the potential of the country to become a major oil producer. The Liza field is due to start up in 2020 via the 120 kbbl/d capacity Liza Destiny FPSO which will be followed by a series of other FPSOs on the block.

In contrast to these positive areas of growth, there are several key producing countries facing major production challenges. Venezuela remains in disarray and is expected to continue to see production decline, with crude output of just 644 kbbl/d in September 2019 compared to 1.9 mmbbl/d in 2017. Furthermore, regional conflict in Syria and Yemen continues to weigh on production there, wiping out substantial supply. Similarly, Libya remains unstable with relatively high production outages.

US sanctions have contributed to severe production cuts in Iran, particularly following an announcement that all sanctions waivers would be rescinded. Before the removal of the waivers, Iranian production had already dropped, with Q4 2018 production averaging 0.7 mmbbl/d lower than Q1 2018. In 2019, crude oil production has decreased by 566 kbbl/d between January and September, and barring a significant change in US foreign policy, this decline is expected to continue across the forecast.

This report includes data and analysis for more than 70 of the most important energy producing countries (covering >99% of global hydrocarbon supply), including detailed drilling and production forecasts for each country covering the period 2019-2025. For this edition of World Drilling & Production Market Forecast, Westwood has added seven new countries to the coverage (Cyprus, Ivory Coast, Kenya, Morocco, Niger, South Sudan, Timor-Leste).

For more information on the latest World Drilling & Production Market Forecast please contact Gareth Hector or request a live demonstration of the Sectors platform here.