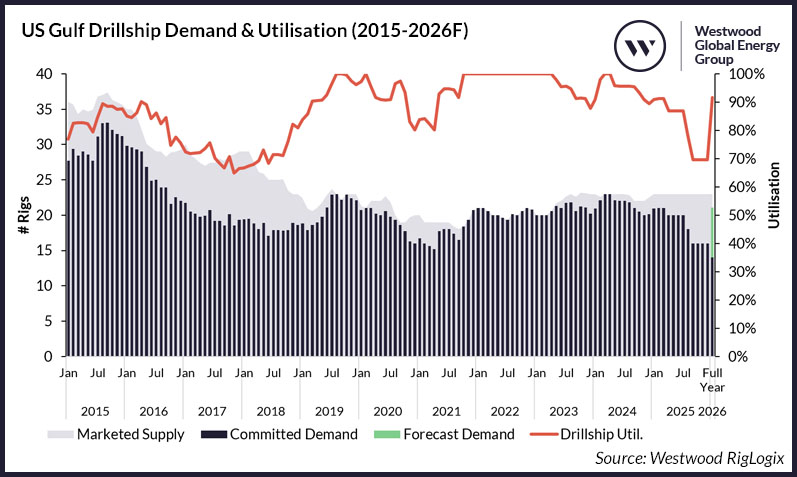

The US Gulf drillship sector is facing a lull in activity not seen since 2018. With marketed utilisation for this segment staying above 90% since mid-2021, near-term availability in the region has been very tight. For the period from October 2021 through April 2023, marketed utilisation stood at 100%. As of early March 2025, marketed committed utilisation, which Westwood defines as units available for work that are either currently under contract or have a future contract in place, is 91% for drillships in the US Gulf. However, several units are poised to roll off charter this year without follow-up jobs lined up yet. This pending drop-off in activity is steep and could see the region’s utilisation rate decrease to 70%.

The US Gulf counts many of the world’s highest specification drillships among its fleet and generally commands some of the highest dayrates in the world for units working in benign waters. The region’s total drillship supply is 23, all of which are marketed. Three of the region’s drillships are 6th generation units, and two are the world’s only 8th generation drillships outfitted with 20,000psi BOPs and other equipment for high-pressure, high-temperature wells. The other 18 are 7th generation units. Drillships used in the region tend to have high hookloads, dual 7-ram BOPs configured to meet US regulatory requirements, and dual activity drilling, among other capabilities.

Idle high spec units

At present, two ultra-deepwater drillships – 7th generation Deepwater Invictus and 6th generation Noble Globetrotter II – are not working. However, Deepwater Invictus is undergoing preparations ahead of starting its next three-year contract in April 2025. Meanwhile, Noble Globetrotter II last worked in April 2024. Additionally, 6th generation drillship Noble Globetrotter I is currently firm until around April, but it has pending options that could keep it going into August, placing it in danger of becoming idle this year, alongside sister rig Noble Globetrotter II. Noble Corporation recently noted that it has effectively removed these two units from competing for drilling work, instead focusing on bidding the two rigs into well intervention programmes and other select opportunities.

7th generation units Deepwater Conqueror and Noble Valiant are also facing idle periods potentially starting around April, although Deepwater Conqueror already has another job lined up with a target start date in October that will keep it working for another year, leaving a gap of several months between its assignments. Next, 7th generation units Noble BlackRhino and Valaris DS-18 are both due to roll off hire around August, followed by West Vela and Stena IceMAX in September. None of these have confirmed new work as of the time of writing.

Should the region reach the fourth quarter with seven units off-hire, this would drop the marketed utilisation rate to 70%. The last time US Gulf drillship utilisation was this low was in mid-2018, which was during the extended global industry downturn. At the time, the marketed supply was a little higher than now at 25 units, and the committed count was 17.

US Gulf Drillship Demand & Utilisation (2015-2026F). Source: Westwood RigLogix

Because the drillships in the region have such high specifications, moving them to other regions would typically result in them not using their full capabilities, thereby lowering the dayrate potential they can command in the US Gulf. Currently, global demand outside the region does not support an influx of very high-specification drillships for term work. Therefore, we expect most of the units that roll off charter in the US Gulf this year to remain in place for opportunities on the horizon for 2026. Market chatter currently suggests the region may see the departure of one of the lower-specifications units, if new work in the US Gulf is not confirmed.

Why the dip in demand?

So, what is contributing to the sudden near-term gaps for so many units? A combination of factors that we are seeing globally and locally have led to what should be a short-term dip in activity in the US Gulf region. These include rising overall project costs (not just rig dayrates) and continued supply chain challenges that mean some long-lead items are taking longer to arrive, resulting in adjusted project schedules to better align development drilling with development equipment installation.

Further complicating the landscape in the US Gulf is the shrinking number of active operators. In 2015, there were 17 active operators that used one or more drillships during the year. By comparison, in 2024, the total number of active drillship operators had dropped to nine. Some of these operators have been swallowed up in various mergers and acquisitions, while others transitioned to onshore portfolios, and others simply are not currently undertaking an offshore drilling campaign.

Additionally, we should consider 2015 semisub demand, which was 12. Over time, operator preference in the region has shifted primarily to drillships when it comes to floating rig selections. Currently, there is only one active semisub working in the region. When reviewing the list of active semisub operators in 2015, an additional eight companies not previously counted on the drillship list are added, although not all these are surviving entities today.

While some operators with pending plug and abandonment obligations may see this near-term white space as an opportunity to seek a rig at a more attractive rate, having fewer active operators means a decreased likelihood of several coming forward to take advantage of potentially lower-priced gap-filler slots. Further challenging the 2025 schedule is that operator budgets for this year have already been set, leaving little wiggle room for unplanned drilling programmes. Furthermore, most operators are already looking to their plans for 2026 and beyond.

2026 demand outlook

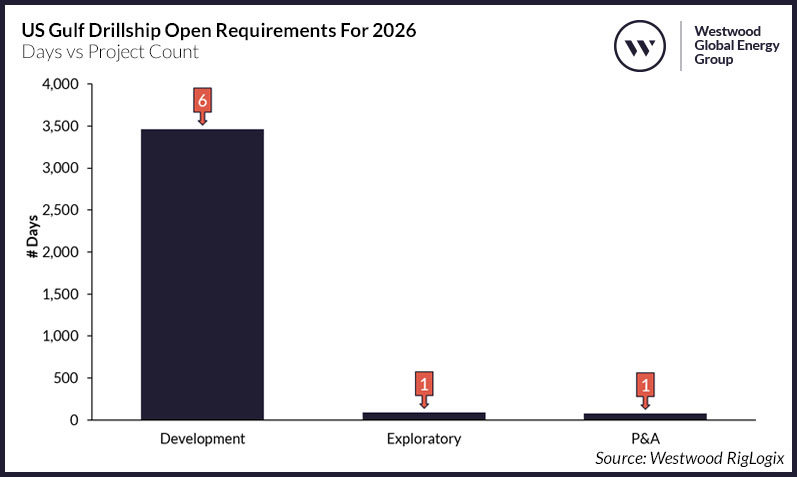

This brings us to our 2026 demand outlook for US Gulf drillships. Westwood’s RigLogix database is currently tracking over 3,600 days of work with target start dates in 2026. The majority of this is expected to be against the renewal of rigs rolling off charter, rather than incremental work. Because some of the region’s smaller independent oil companies tend to run rig lines of between one and two units per year, some gaps between assignments are expected. However, as noted earlier, having fewer active operators in the region reduces the number of companies that may emerge with unanticipated new requirements.

US Gulf Drillship Open Requirements For 2026. Source: Westwood RigLogix

While the second half of 2025 will be challenging for US Gulf drillships that roll off charter, most are expected to ride out the rough waters in anticipation of more work in 2026 and a return to tight utilisation. Longer term, the US Gulf will remain one of the top locations in the world for drillship activity.

Cinnamon Edralin, Americas Research Director

[email protected]