The UK and Norway oil and gas sectors experienced very different years in 2024, and these differences are only expected to further diverge going forwards. In the UK, a change in Government, the October Budget and resultant changes to the EPL dominated the sector in 2024. Although the industry might now see some fiscal stability, frustration amongst the industry continued with even more support taken away from an already struggling sector. 2024 saw the fewest M&A deals announced on the UKCS since pre-2010 and the lowest ever number of exploration well completions. Development activity was also low with only two fields gaining regulatory approval and just one field starting production.

In contrast, Norway remains Europe’s largest oil and gas producer and a key supplier of energy to the continent. In 2024, the country remained firmly in development mode after the huge wave of project sanctions in 2023, and unsurprisingly there was little in terms of new project sanctions. Although E&A activity remained buoyant, with 29 exploration well programmes completing, discovered volumes were relatively low.

UK: Three key consultations in 2025 could shape the future of the UK industry

Production is forecast to rise by 3% in 2025 to 1.14 million boepd, with full year production from the Talbot field and contributions following the start-up of the Penguins, Affleck, Jackdaw, Murlach, Victory and Teal West fields. However, the increase is more a result of project delays than an uptick in investment. Post-2026, production is expected to enter a steep decline as the impact of under-investment takes effect. Fields without submitted EIAs are unlikely to gain approval in 2025 due to the lengthy review process. Currently, only Avalon and Buchan Horst have EIAs under consideration, but due to the lack of reported progress on them, it is unclear whether either will gain sanction in 2025.

The number of field and hub closures is on the rise, with eight hubs expected to cease this year. As a result, companies are expected to spend US$2 billion on abandonment activities in 2025, with total abex spend over the next decade (2025 – 2034) estimated at over US$26 billion. The next five years are crucial in maximising recovery from the high number of late-life hubs across the UK, but based on existing investment plans, Westwood forecasts the number of hubs to reduce to 46 by 2030, 20 by 2035, with only four remaining in 2040.

Figure 1: Westwood’s forecast of fields in production in 2024, 2030, 2035 and 2040, based on current investment plans. Source: Westwood Atlas

E&A activity in 2025 has the potential to pick up from 2024 when just one appraisal and three exploration wells completed. Westwood currently has visibility of 10 exploration wells that could operate this year with pre-drill resources of c. 545 mmboe. However, with the ongoing fiscal and political uncertainty in the UK, investor appetite has been impacted and there is a high chance that many of these wells will not be drilled in 2025. All but one of the planned exploration wells are in the Central North Sea, with Dabinett the only well planned in the Southern North Sea. There is also the potential for three appraisal wells, appraising a midpoint volume of c. 230 mmboe.

Three key consultations in 2025 could shape the future of the industry. The consultation on Environmental Impact Assessments and the inclusion of Scope 3 emissions closed on 8 January with new guidance expected in Spring. Perhaps the most pivotal for investor sentiment is the consultation on licensing that could set out the Government’s appetite for future exploration and potential new developments. The third consultation is on the fiscal regime post-2030, which could have a significant impact on project economics, particularly for near-term developments.

The M&A market in 2025 is poised for more activity than the 13 deals announced in 2024, encouraged by a degree of fiscal certainty and numerous assets for sale. After the significant 2024 mergers of Shell-Equinor and Ithaca-Eni, there are fewer remaining large company merger opportunities, but can expect smaller corporate transactions and more asset deals taking precedence in 2025. Tax efficiencies will likely be the key driver of M&A activity in 2025, with portfolio optimisation also playing a significant role.

Norway: The sector remains firmly in development mode, but new opportunities need to progress to minimise future production decline

In 2025, Norway will continue to be Europe’s key supplier of energy. Production is forecast to rise to 4.2 million boepd in 2025 following the start-up of seven new field developments and four brownfield projects, totalling 1.1 bnboe in reserves. Equinor’s delayed Johan Castberg field is the largest, which is now expected online in Q1 2025.

The country remains firmly in development mode after the wave of project sanctions following the introduction of the temporary tax terms in 2020 – 2022. With operators focusing on delivering these projects, there has been a lag in the number of firm new development projects moving forward for FID. Only seven new field developments in three greenfield projects are expected to be sanctioned in 2025, with combined reserves of c. 225 mmboe. Opportunities, however, do remain and a forecasted production decline later in the decade is expected to be stemmed through investment in existing assets, new developments and sustained exploration. This will be crucial to maintain supply to meet European energy demand. However, managing activity and ongoing supply chain inflation will be key to protecting project economics.

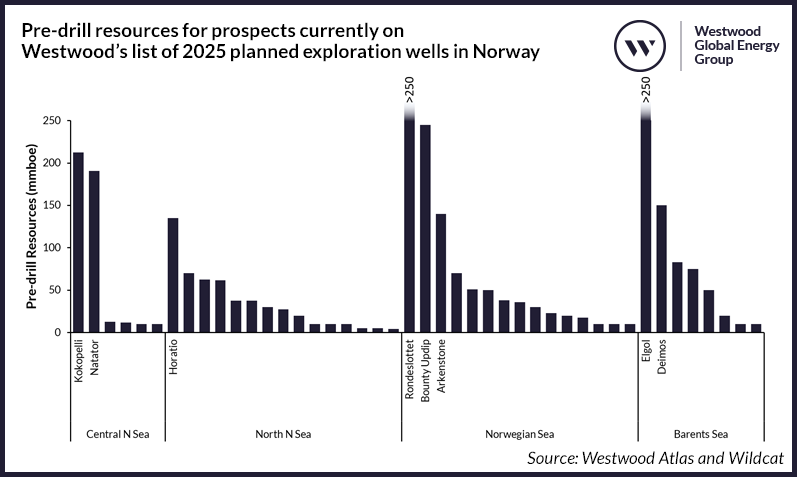

High levels of E&A activity are expected to be maintained in 2025. There are 44 exploration wells currently on Westwood’s list of planned wells with associated pre-drill resources of c. 3.2 bnboe (Figure 2). Many of these have been deferred from 2024 due to rig schedules. Historically, the Northern North Sea has been the most drilled basin, but in 2025, the Norwegian Sea and NNS both have 15 planned wells. Pre-drill resources, however, in the Norwegian Sea are three times higher than in the NNS. All wells in the NNS are infrastructure-led exploration whereas three wells in the Norwegian Sea are considered to be high impact. There is a continued focus on Barents Sea exploration, with eight planned wells. In addition, there are 4 appraisal wells appraising a midpoint volume of at least c. 145 mmboe.

Figure 2: Pre-drill resources for prospects currently on Westwood’s list of 2025 planned exploration wells in Norway (Note: only high impact wells are labelled. Elgol has been completed dry). Source: Westwood Atlas and Wildcat

There are relatively few companies operating in Norway and therefore there are a limited number of acquisition opportunities, making it a sellers market. The M&A market will be driven by portfolio optimisation with some larger players rationalising their portfolios and offloading non-core assets. This could include companies with assets that are late life or have high emissions intensity, or companies that have made recent corporate acquisitions. Those with portfolios weighted to assets under development may look to farm down their interests to reduce development exposure and small pre-development led companies look to acquire a production revenue stream.

UK and Norway oil and gas: two disparate basins

For two regions that share a median line, the post-COVID policies for the UK and Norway oil and gas sectors could not be more different. The UK introduced and has maintained a windfall tax which has detrimentally impacted an already challenged mature industry. Norway, which is a less mature region, not only maintained its investment levels but stimulated capital spend. With three consultations due to take place in the coming months, the UK could learn from Norway’s strategies to maximise economic recovery from the oil and gas sector and not just place more burden on operators that will stifle future investment.

Emma Cruickshank, Head of Northwest Europe

[email protected]

Stephen Coomber, Senior Analyst – Northwest Europe

[email protected]

Glenn Morrall, Senior Analyst – Northwest Europe

[email protected]

Matthew Belshaw, Analyst – Northwest Europe

[email protected]

In response to increased decommissioning activity, Westwood is launching a new Atlas Decommissioning module in 2025. For further details, please contact [email protected].