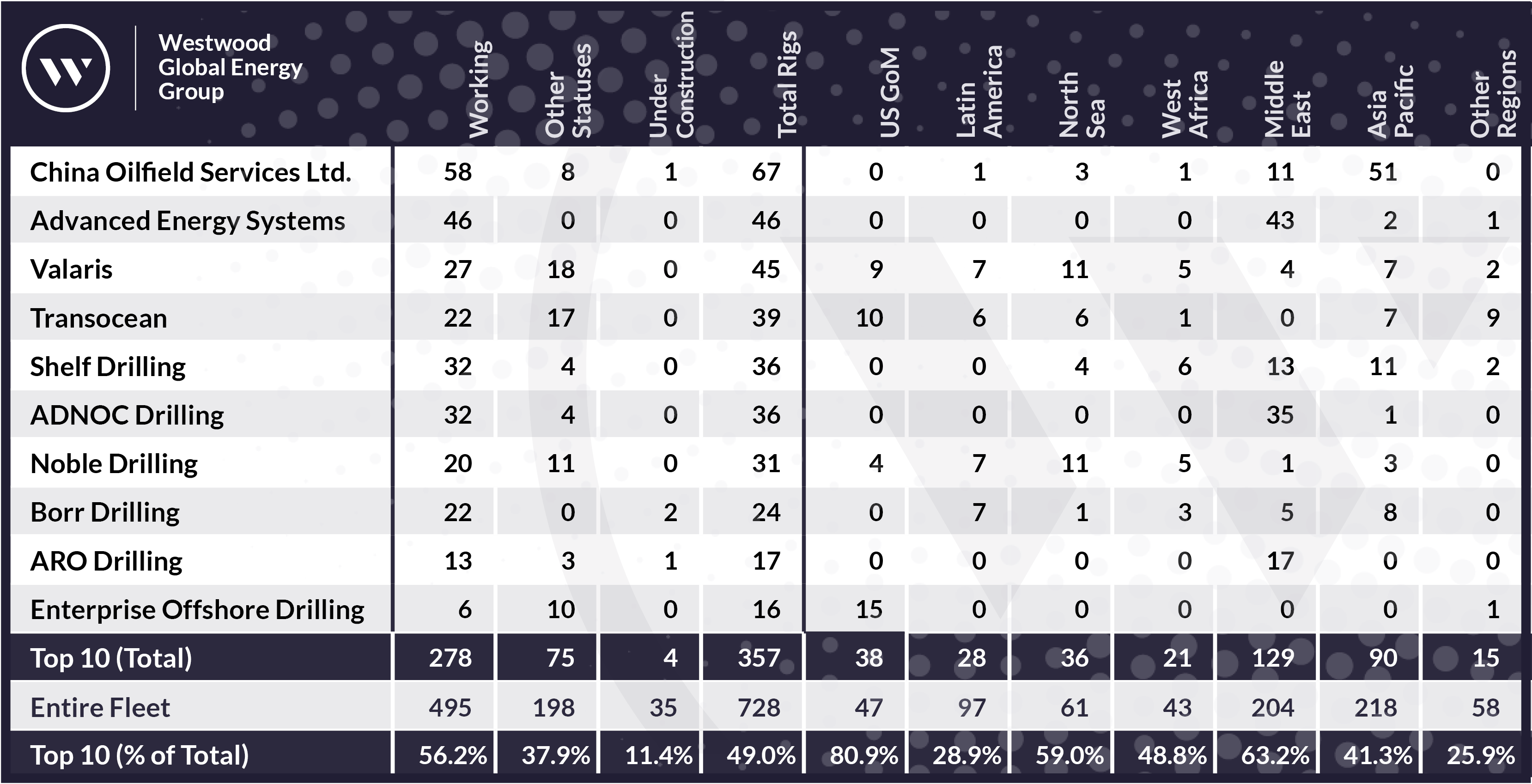

This article was originally published in Offshore Magazine on 11 June 2024.

The global offshore drilling rig fleet of jackups, semisubmersibles (semisubs) and drillships kept busy in 2023, returning more rigs to work and delivering several formerly stranded newbuilds that had been held up in the construction process during the prolonged downturn. Over the year, China Oilfield Services Ltd. (COSL) expanded its fleet and retained the title of largest rig contractor in terms of managed rig fleet size with 67 units. In addition to relinquishing management of a few non-owned units and picking up management of another, COSL also acquired four newbuild jackups that had been stranded at Dalian Shipbuilding for a reported price of US$446 million. The four Friede & Goldman JU-2000E design jackups (now known as Hai Yang Shi You 945, Hai Yang Shi You 946, Hai Yang Shi You 947 and Hai Yang Shi You 948) had originally been ordered by Seadrill in 2013; however, the construction contracts were terminated in 2018 and 2019.

Rounding out the top three, Valaris and Advanced Energy Systems (ADES) switched places, with Valaris dropping one unit to 45, slipping it into third place, and ADES moved into second place after increasing its managed fleet size by one to 46. Valaris agreed to sell the jackup now known as Admarine 11 (ex-Valaris 54) to ADES in 2022, with closing to take place after the rig finished its contract in March 2023.

One name it may be a surprise not to see on the list is Seadrill. However, Seadrill has a number of arrangements in place that result in the rig contractor having several rigs managed by other companies. As of the end of 2023, the company owned 19 rigs, three of which are leased to the GulfDrill joint venture (JV) for which operations are managed by Gulf Drilling International, and one of which is leased to the Sonadrill JV. The Sonadrill JV is managed by Seadrill and also holds two rigs owned by partner Sonangol.

Furthermore, Seadrill drillship Capella is managed by Vantage Drilling, and drillship Vela is managed by Diamond Offshore. Drillship West Auriga was being managed by Diamond at the end of last year but has since transitioned to Seadrill management. Meanwhile, management of Capella and Vela will be handed over to Seadrill upon completion of their respective charters.

Top 10 Offshore Drillers

Source: Westwood RigLogix (Data as of 31 December 2023)

Global demand ramping up

According to data from Westwood’s RigLogix, the global offshore rig fleet size ended 2023 at 728 jackups, semisubs and drillships, down by a net one rig from the end of 2022. This is a considerable slowdown in supply shrinkage over the past several years. Strong demand is reducing the pressure on rig contractors to decrease supply. Sales for scrapping and conversions have slowed considerably. Instead, the market is seeing an increase in idle units being reactivated. The number of rigs actively working at the end of 2023 was up by 33 over the prior year. The 10 largest managers controlled 56% of the working units globally.

In addition, the number of offshore rigs under construction dropped by nine, and the number of rigs with other statuses, which includes stacked rigs and rigs at shipyards, decreased by 25. Of the remaining rigs under construction, only 11% are managed by the top 10 managers. All nine of the rigs delivered in 2023 – six jackups and three drillships – are managed by one of the 10 largest managers.

Seven of these nine have secured work. The two rigs delivered in 2023 that do not yet have work are ultra-deepwater drillships Valaris DS-13 and Valaris DS-14. Valaris had purchase options for these two rigs well below current valuations for DSME 12000-design drillships, at US$119 million for Valaris DS-13 and US$218 million for Valaris DS-14. With the average leading-edge dayrate for 7th generation drillships at about $460,000 in December 2023, these rigs were priced too well to pass up. Both units are currently warm stacked in the Canary Islands and will need to be reactivated upon securing work.

2023 ended with nine more drillships, three more semisubs, and 21 more jackups working than at the end of 2022. The Middle East was the primary driver of the double-digit increase in jackup demand, growing from 138 to 170 as the region looked to support production initiatives. The regions with the biggest drops in jackup demand were Asia Pacific, down six, and the North Sea, down four. The UK has experienced a continued drop in demand for both jackups and semisubs partly in response to the Energy Profits Levy, which was introduced in 2022 and is now set to expire in March 2028 after initially being set to expire in December 2025. As a result, some rigs have left the region for opportunities elsewhere.

Top 10 dominate several regions

In terms of region, the top 10 contractors continue to dominate the US Gulf of Mexico, the North Sea, and the Middle East, with over half the total fleets managed by this group. West Africa is just below half at 49%. The region where the top 10 had the strongest presence at the end of 2023 was the US Gulf of Mexico at 81%, with Enterprise Offshore managing the most rigs at 15. However, most of Enterprise’s fleet is stacked and not being marketed for work at this time. Transocean has the second largest fleet in the region, but it has the most working rigs.

The Middle East is the largest region in terms of rig supply, and here the top 10 make up 63%. The number of Middle East-based contractors and their rig counts have been increasing in recent years as local contractors have been building their fleets. ADES and ADNOC are the largest by far, with 43 and 35 rigs, respectively. Of the six jackups delivered last year, two went to ADNOC Drilling, and one went to ARO Drilling. The other three were for COSL.

Even with the drop in demand in the North Sea region and subsequent rig moves to other regions, the top 10 contractors still accounted for 59% of the total fleet in the region at the end of last year, with Noble and Valaris each managing 11 rigs. In West Africa, Shelf Drilling manages the most rigs at six, followed by Valaris and Noble each with five.

In Asia Pacific, which is comprised of the Far East, Southeast Asia, South Asia and Australia, COSL is the biggest player, managing 51 units. Nearly all of COSL’s rigs in the region are concentrated in China, and the remaining few are in Indonesia and Malaysia.

Turning to Latin America, the top 10 contractors managed only 29% of the rigs in the region, with a three-way tie at seven rigs each for Valaris, Noble and Borr Drilling. Noble’s fleet is mostly concentrated in Guyana, where it had four drillships working at the end of last year. Additionally, one semisub was working off Colombia and one drillship off Trinidad and Tobago, while a second semisub was located off Trinidad and Tobago while it prepared for its early 2024 campaign off Suriname. For Borr, all seven of its Latin America jackups were working offshore Mexico. Meanwhile, Valaris had four drillships working off Brazil, one jackup off Mexico and two off Trinidad and Tobago.

In the Latin America market, there are several local contractors that are major players in each country. In Brazil, Constellation Oil Services with seven rigs and Foresea with six are the largest managers in the country. The biggest company from the top 10 list is Transocean, which had five rigs in Brazil at the end of 2023. In Mexico, local contractor Perforadora Central and top 10 company Borr are tied with seven units apiece, followed by local player Perforadora Mexico with five rigs.

Within Latin America, there is a strong preference to work with local entities, making it difficult for international companies to build their presence. However, the increased demand within the region has been an opportunity for additional international rigs to move in.

Looking forward

What does Westwood anticipate for year-end 2024? Once again, we should see a drop in the number of rigs under construction, with some deliveries expected and no new orders being added to the count. Rig contractors are currently more focused on selective asset acquisition rather than full-company mergers, so the Top 10 list next year is likely to show more position changes than names moving on or off.

In terms of the working rig count, the drillship figure should rise as some rigs complete their reactivations or final construction activities and start previously awarded jobs. Meanwhile, the working semisub count is poised to end lower as several units roll off charters this year without enough near-term opportunities to see them all back to work before the end of 2024. Additional work is expected to emerge in 2025, but one or more of the idle semisubs may be cold stacked to reduce costs and competition within this segment. Jackups may also show some near-term softness, with Saudi Aramco reportedly suspending 20-25 units for periods up to one year, not all of which may be able to transition to new jobs by the end of this year.

In terms of regions, Latin America and West Africa are expected to grow their floater counts, while the Middle East will remain the biggest driver of jackup demand, despite the Saudi Aramco suspensions.

Cinnamon Edralin, Americas Research Director

[email protected]