This article was originally published in Offshore Engineer Magazine.

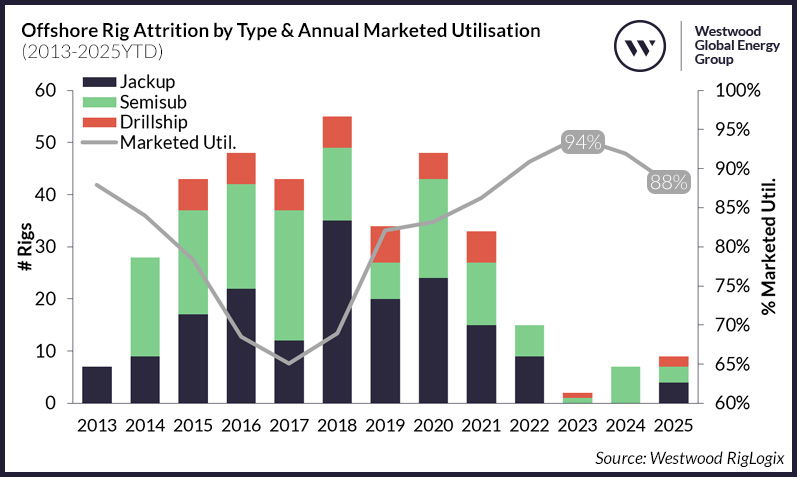

The offshore rig market recovery appears to have taken a pause, with demand tapering off and marketed utilisation hitting the lowest levels recorded since recovery began in 2021. A variety of factors have contributed to this – including Saudi Aramco’s suspension of over 30 jackup contracts by up to one year, the entry of newbuild rigs into the market without work to go to, and the deferment of several long-term deepwater drilling and plug and abandonment projects.

The unexpected combination of a dip in firm demand (currently 18% lower versus March 2024) and an increase in supply (7% higher than March 2021), has seen marketed utilisation fall to 88% as of March 2025 – representing a 6% drop in less than two years.

We’re only three months into 2025 and attrition this year is the highest it’s been since 2022. Additionally, with Westwood predicting utilisation of the combined jackup, semisub and drillship segments to fall further this year to around 85% – it seems likely that more rigs could permanently be removed from the active drilling fleet as the year progresses.

Figure 1: Offshore Rig Attrition by Type & Annual Marketed Utilisation (2013-2025YTD). Source Westwood RigLogix

As has historically been the case, when utilisation is high and the availability of marketed rigs is tight, the probability of stacked rigs being reactivated is more likely. This explains why attrition began to fall in 2021 and shrunk to near nought by 2023, when utilisation was the highest it has been in the past decade. However, during the sustained downturn which ran from 2014 through to 2018, before a slight recovery in 2019 (until Covid-19 hit in 2020), the number of rigs being retired or sold for purposes outside of the active drilling market was particularly high – averaging around 43 rigs per year over the 2014-2020 period.

Last year, attrition started to pick up again as market softness began creeping in, especially in the UK North Sea semisub market, where four of the seven assets were retired.

Year to date, nine rigs have been confirmed for removal from the active fleet. These consist of four jackups – owned by Shelf Drilling, White Fleet Drilling and Well Services Petroleum – and three 8500-series semisubs owned by Valaris, all of which were under 15 years old. Additionally, Noble confirmed the disposal of two modern S12000-design, ultra-deepwater drillships that it inherited during its acquisition of Pacific Drilling – one of which never drilled a single well and was just 10 years old.

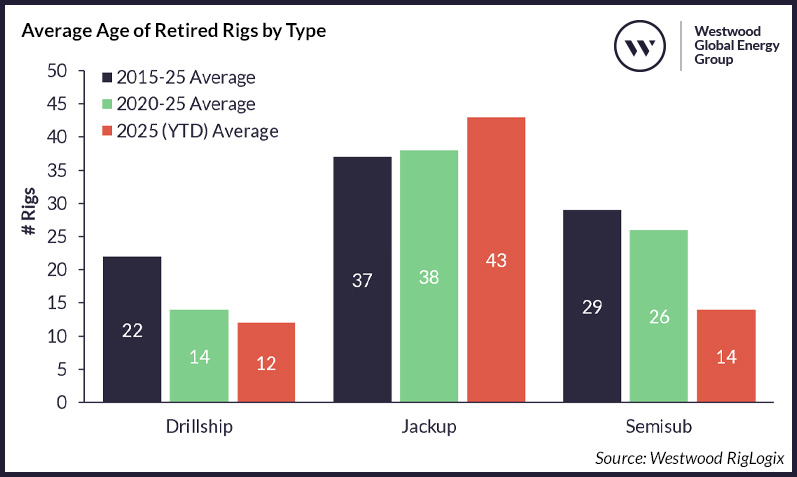

Figure 2: Average Age of Retired Rigs by Type. Source Westwood RigLogix

The average age of assets retired from the fleet has continued to reduce for floating rigs, with drillships reducing by eight years over the last five years, and semisubs reducing by three years. However, jackups have not followed the same pattern, with a slight increase recorded during the same period, of a one-year increase in average age of attrition. For the four assets confirmed for removal year to date, this figure is significantly higher at 43 years old.

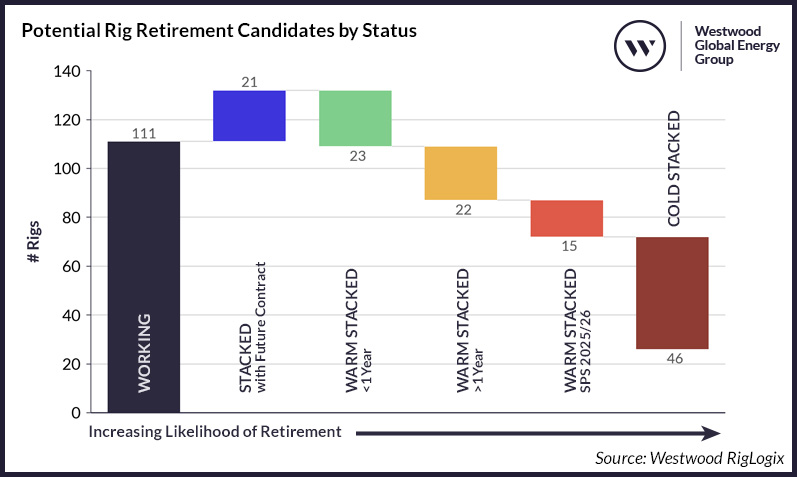

Of course, falling utilisation and age are not the only factors to sway the likelihood of a rig finally hitting the scrap heap, and in fact RigLogix records 87 units over 40 years old that are still currently drilling. Generally, rigs that have limited future prospects, have been without work or cold-stacked for some time (meaning a costly reactivation programme), and are due the often very expensive five-yearly special periodic survey (SPS), are also considerations.

Other factors can be one-off designs in a contractor’s fleet, where they may not be able to spread spare parts costs etc, out-of-favour designs (as seen with the small variable deck load on the 8500-series semisub), and of course mergers between owners, which often enables easier culling decisions as owners look to streamline fleets.

Figure 3: Potential Rig Retirement Candidates by Status. Note: Includes jackups over 38 years, drillships over 14 years and semisubs over 26 years. Source Westwood RigLogix

Figure 3 indicates that there are certainly more candidates that could be considered for removal over the coming year, when taking into account the average rig attrition age during the 2020-25 period alongside the status, stacked duration and SPS due date.

For jackups, 39 of these units are cold stacked and 19 are warm stacked (seven of these for over a year). Eight of these warm assets do not have a valid SPS in place and three more will expire this year or next if not renewed. Most of the units included in Westwood’s analysis are located in the Middle East, India or US waters, with Shelf Drilling and Enterprise Offshore owning most of these rigs.

For drillships, there are just five cold-stacked assets, all between 14 and 16 years old. There are seven warm or hot stacked units (none of which have been idle for more than a year) and four of these do not have a valid SPS, or it will expire in 2025 or 2026. Most of the drillship candidates are in Southeast Asia or the Mediterranean, with Transocean, Seadrill, Stena, Vantage and Saipem owning these assets.

Finally, for semisubs, the pool for candidates (based on the above factors) is small – primarily due to the high level of attrition already undertaken in the segment over the past decade, which has resulted in total supply of the fleet reducing by 59% (119 rigs) since March 2015. There are only two cold-stacked and three warm-stacked assets. Just one of the warm units has been idle for over a year and, all but one rig, either do not have a valid SPS, or it will expire in 2025 or 2026. However, two of these assets are located in the land-locked Caspian, where bringing in new rigs is a challenge and therefore makes them less likely to be scrapped. The remaining assets are currently in Las Palmas (Canary Islands), the North Sea or Canada and are owned by Dolphin Drilling, Well-Safe and Transocean. The combination of the reduced pool of retirement candidates and the ongoing softness in demand means an increased chance of a younger, hotter unit being retired.

To sum up, due to the reduction in jackup, drillship and semisub demand and utilisation this year, we will likely see more assets moved to cold stack due to not having follow-on commitments in place. Meanwhile, further M&A activity could also be in the works.

These factors we believe will spur further older, idle and surplus assets to be removed from the fleet, which in the long run may help set the stage for a stronger recovery in utilisation from the second half of 2026 onwards, when Westwood expects to see a rebound in demand.

Teresa Wilkie, Director – RigLogix

[email protected]