Hydrogen is a key component of Europe’s decarbonisation and net zero ambitions. Individual countries and the EU have published hydrogen strategies – setting ambitious capacity and demand targets. A number of projects have been announced across Europe’s major markets[1], with a current pipeline capacity of 111.5GW (LHV) as assessed by Westwood.

Europe is driving the development of hydrogen through significant funding and subsidy mechanisms at a regional and country level, notably the Important Projects of Common Interest (IPCEI) and the EU Innovation Fund with €18.9 billion and €4.8 billion allocated respectively. Some countries have developed domestic support mechanisms, such as the UK’s CfD-based Hydrogen Allocation Round (HAR) and Germany’s flagship funding scheme H2Global.

However, despite the European focus on and support of hydrogen, the emerging industry has experienced growing pains in the past year, culminating in the cancellation and stalling of several projects.

A fifth of projects lost

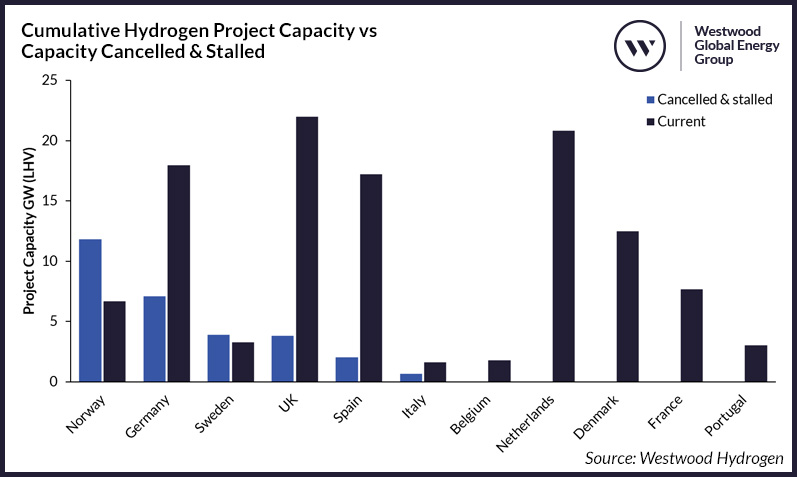

Westwood has identified 23 projects in the European pipeline that have been classed as cancelled or stalled across 11 major European countries that make up the majority of the Hydrogen opportunity. The total capacity impacted by these projects is 29.2GW (LHV) – the equivalent of 20.3% of the pipeline when considering all project statuses (current, cancelled and stalled).

Cumulative Hydrogen Project Capacity vs Capacity Cancelled & Stalled

Source: Westwood Hydrogen

Across these countries the amount of capacity ‘lost’ varies greatly, with the Netherlands unaffected through to Norway, which has lost more capacity than it has remaining in its pipeline, 11.8GW (LHV) and 6.7GW (LHV) respectively.

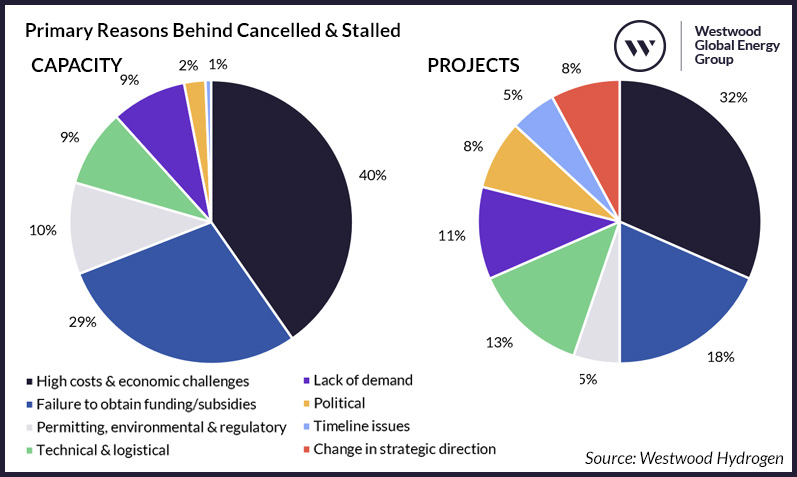

To better appreciate what countries must act on to prevent further cancellations, it is important to understand the challenges hydrogen projects are facing. There are often multiple reasons for project cancellations or delays, but to help focus our analysis Westwood has explored three primary reasons given by projects. These are considered to be high costs and economic challenges, failure to obtain funding and lack of demand.

Primary Reasons Behind Cancelled & Stalled Capacity/Projects

Source: Westwood Hydrogen

1. High costs and economic challenges

The elevated cost of projects hampering development has been a recurring trend for the last few years. Westwood has attributed high costs and economic challenges to 32% of projects (and 40% of capacity), with Norway by far the most impacted country: losing 10GW of potential capacity from Equinor’s cancelled CCS-enabled and electrolytic Clean Hydrogen to Europe projects. These projects required a pipeline to be constructed to Germany, which was subsequently cancelled due to the cost of not only the pipeline but also the CCS-enabled hydrogen facility. Equinor stated the cost to be in the “tens of billion euros”[2].

Developers have highlighted that if significant funding is not obtained alongside cost reductions across the supply chain to counteract the higher costs, more developments will be halted.

2. Failure to obtain funding

The failure to obtain funding is a further reason for 18% of projects (and 29% of capacity) to stall or be cancelled, including in many cases a lack of clarity on how to compete for funding in the future.

Across the UK and Germany this has inhibited over 8GW of projects developing, one of which being the huge 1.8GW (LHV) DepHYnus project that was unable to win funding in the Hydrogen Allocation Round (HAR) within the UK. The developers stated that the project was cancelled as a result. This is one of multiple symptoms of the HAR round, with developers finding the process long and confusing and the CfD mechanism being much more complex than its offshore wind counterpart. Additionally, some developers selected in the HAR processes have pulled out, citing the challenges around timelines. This means that despite projects being deemed worthy of funding they are still not able to proceed.

3. Lack of demand

Another common challenge faced is the lack of demand, with 11% of projects (and 9% of capacity) lost, citing this as the reason for shelving their projects. The inability to secure demand is a key reason projects are unable to secure any finance.

One prominent example of this is from within the Sustainable Aviation Fuel (SAF) sector, with over 0.7GW (LHV) of capacity being cancelled or postponed in Sweden alone. Developers are finding the market insufficient in an industry where SAF is the only viable path to decarbonisation, raising concerns about the effectiveness of existing EU guidelines and mandates. While the RED III directive is binding across Europe, it will require action from governments at a national level to ensure it is met. Similarly, the ReFuel EU – Aviation mandate requires a 2% share of SAF at EU airports by 2025, increasing to 70% by 2050. However, despite these initiatives, there remains a lack of support for offtakers to commit to early, high-price (and long term) agreements, suggesting the current strategy is not robust enough.

Key conclusions

Europe’s hydrogen ambitions remain at a crossroads, with a mix of bold targets and various funding schemes on one side and mounting project cancellations and delays on the other (the impact of which varies across the region).

While strides have been made in setting the stage for a hydrogen-supported energy transition, the delay and cancellation of 29.2GW (LHV) – 20.3% – in project capacity highlights the fragile state of the sector. High costs, insufficient demand and funding uncertainties remain formidable barriers, exposing gaps in current strategies with some countries struggling significantly more than others.

If Europe is to meet its electrolyser capacity goals and realise hydrogen’s potential, a new approach is essential, balancing ambitious targets with realistic cost structures, robust market incentives (for supply and demand), and clear funding mechanisms. Hydrogen can play a significant role in the future, but without addressing its present challenges, it risks stalling before it truly takes off.

Ben Clark, Senior Analyst – Hydrogen & CCUS

[email protected]