The Norway State of Exploration report analyses exploration activity and performance of wells that have been drilled on the Norwegian Continental Shelf (NCS) between 2014 and 2023, as well as the results to date for 2024 and an outlook for the remainder of the year.

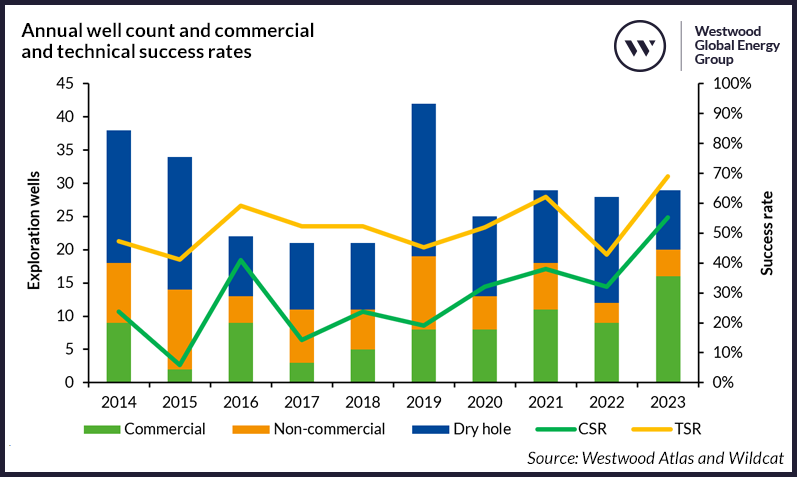

A total of 289 wells were drilled and completed on the NCS between 2014 and 2023, at an estimated drilling cost of US$12.1 billion. Eighty commercial discoveries were made with total resources of 2.5 bnboe, at a drilling finding cost of US$4.8/boe. The average commercial success rate (CSR) was 28% for the decade but varied from a low of 6% in 2015 to a high of 55% in 2023 (Figure 1).

Figure 1: Annual well count and commercial and technical success rates. Source: Westwood Atlas and Wildcat

There has been a general upward trend in CSR since 2015 which correlates to an increasing proportion of infrastructure-led exploration (ILX) wells being drilled, as companies look to sustain production levels in older hubs and improve project economics and cycle times. ILX drilling accounted for c. 70% of all activity and spend and contributed 2.2 bnboe with a CSR of 36%. Only seven commercial discoveries were made from 100 high impact wells during the decade, with associated resources of c. 555 mmboe, of which only two made a discovery that was >100 mmboe post-drill.

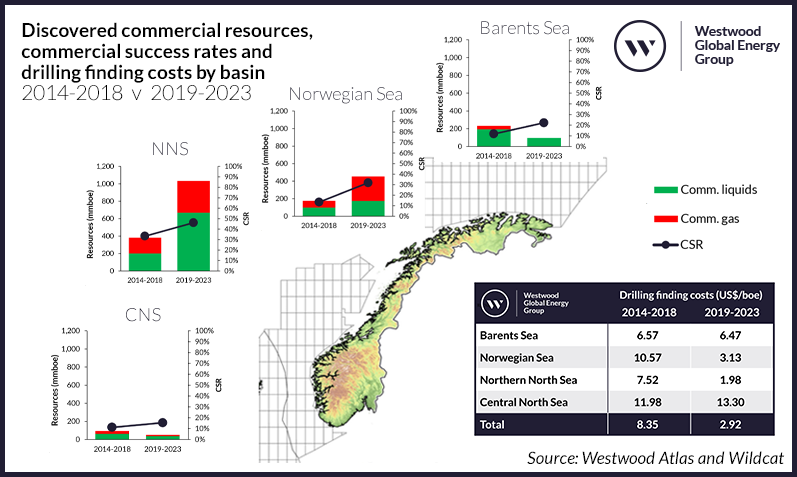

The Northern North Sea not only saw the most exploration through the decade, it was also the best performing basin in terms of commercial resources discovered, CSR and drilling finding cost (Figure 2). The Barents Sea continues to have a low CSR, reflective of the frontier nature of the basin. Despite having the highest proportion of high impact wells, discovered commercial resources were low. Even large discoveries in the Barents are not currently commercial due to the lack of infrastructure and gas offtake solutions.

Figure 2: Discovered commercial resources, commercial success rates and drilling finding costs by basin, 2014-2018 v 2019-2023. Source: Westwood Atlas and Wildcat

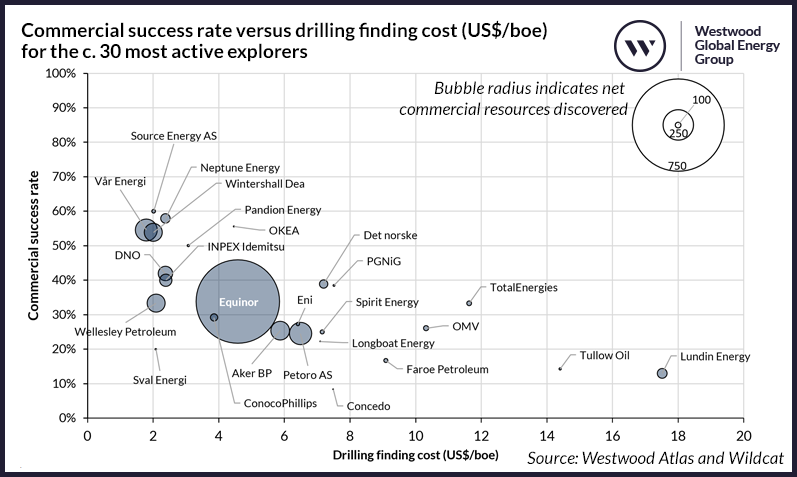

A total of 77 companies participated in exploration drilling. Figure 3 shows exploration performance metrics of the c. 30 most active companies. All but two of these companies made at least one commercial discovery, with an average CSR of 30% and average net commercial resources discovered of 77 mmboe per company. Equinor was not only the most active explorer but also discovered the most net commercial resources. Vår Energi discovered the most net resources of the independent companies, followed by Aker BP, Wellesley Petroleum and Wintershall Dea.

Figure 3: Commercial success rate versus drilling finding cost (US$/boe) for the c.30 most active explorers. Source: Westwood Atlas and Wildcat

Westwood currently holds a pool of 47 exploration wells expected to be operating in 2024 with a combined pre-drill resource of c. 2.85 bnboe. Fifteen wells were completed in the first half of 2024 and although a CSR of 40% has been achieved, discovered volumes are just 86 mmboe with all six discoveries being small. The remaining 2024 wells that are either active or expected to spud in H2 have pre-drill resources of c. 1.8 bnboe and include four HI wells. Looking to 2025 and beyond, Westwood expects that the high proportion of ILX drilling will continue, with less emphasis on HI prospects as the basin matures and there are fewer large play openers. An exception might be in the Barents Sea where there is still potential for large discoveries.

Stephen Coomber, Senior Analyst – NW Europe

[email protected]

Alyson Harding, Technical Manager – NW Europe

[email protected]

Emma Cruickshank, Head of Research – NW Europe

[email protected]

The Norway State of Exploration 2014-2023 report is available now to subscribers of Westwood’s Atlas product. Non-subscribers can purchase the full report by contacting [email protected] or completing the form below.