Iberia is central to the European Hydrogen narrative. Both countries aim to leverage their renewables potential to support the development of sizable electrolytic hydrogen markets – to decarbonise their own economies and also to export to the wider continent. This commitment is reflected in their ambitious 2030 electrolyser capacity targets, which have both been increased in draft plans to 11GW (7.3GW (LHV)) for Spain and 5.5GW (3.6GW (LHV)) for Portugal.

With its ambitious renewable electricity targets, Portugal presents significant opportunities for hydrogen project developers. The country’s grid, which is already approaching 75% renewable on average, is on track to achieve a revised target of 93% by 2030[1]. This progress offers a considerable advantage, as hydrogen projects in Portugal will be exempt from the additionality clause in the EU’s REDII Delegated Act[2].

In Spain, while the 2030 renewable electricity target of 74% does not offer the same additionality exemption benefit, the country’s vast and growing solar energy potential provides access to cheap renewable electricity needed for lower electrolytic hydrogen production costs.

These advantages have already been demonstrated by successful bids in the first European Hydrogen Bank auction, where project developers in both countries showed the ability to design projects that were deemed to be economically viable despite receiving relatively low subsidy support.

Progress in the pipeline

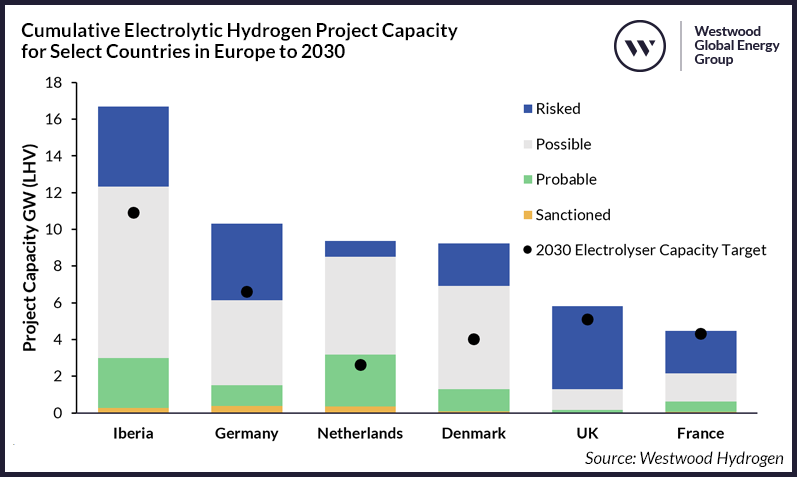

Westwood has identified 16.7GW (LHV) of electrolytic hydrogen projects on the Iberian Peninsula by 2030, more than enough to meet the region’s target. While Spain’s pipeline could potentially exceed its target, Portugal’s current projects fall short of the upgraded 5.5GW (3.6GW (LHV)) target.

Only 1% (262MW (LHV)) of these projects have passed Final Investment Decision (FID), with a further 14% categorised as ‘Probable’[3] and on track for FID. This level of project maturity is comparable to that of other European countries like Germany and France.

Cumulative Electrolytic Hydrogen Project Capacity for Select Countries in Europe to 2030. Source: Westwood Hydrogen

As expected, the majority (87%) of the 16.7GW (LHV) production capacity on the Iberian Peninsula targets industrial decarbonisation and refining, which is a similar theme across major European markets where the initial focus is on replacing existing ‘grey’ hydrogen users, as existing infrastructure can be leveraged for renewable hydrogen projects. This focus is driven in-part by explicit national targets, such as in Spain which is targeting 74% of industrial hydrogen to be RFNBO[4]-compliant by 2030. In Portugal, two projects that have reached FID are located at Bondalti’s Estarreja chemical complex and Galp’s Sines refinery – covering 94% of Portugal’s existing hydrogen demand. Although Iberia is positioned as a potential key export to Europe, significant pipeline and port infrastructure must be developed before substantial exports become a primary focus for project developers.

Securing offtake and electrolysers

Despite the ambition, 77% of projects in the chemicals and refining sectors are categorised as ‘Risked’ or ‘Possible’, primarily due to the lack of offtake agreements (72% of Iberian projects) and uncertainties around chosen electrolyser technology (69%). Offtake agreements are crucial for securing funding and ensuring project bankability as they ensure a long-term revenue stream. Additionally, the absence of purchase orders for electrolysers highlights the immaturity of these projects across the peninsula.

While 48% of Portuguese projects have made some progress on their electrolysers, none have secured offtake agreements leaving much of the pipeline categorised as ‘Possible’. A few announced offtake agreements in Portugal could significantly brighten the outlook for its hydrogen pipeline.

Funding delays

Funding delays in Spain have led major players like Iberdrola and Repsol to scale back their renewable hydrogen production targets. A two-year delay in receiving government funding has already jeopardised some projects, with further delays potentially inhibiting the country’s ability to meet its expansive domestic demand and wider decarbonisation targets.

While Portugal’s domestic funding mechanisms have recently gained EU approval, awards are not expected until the end of 2025. This delay poses a potential risk, as Portugal’s project pipeline consists of only 11 projects with 97% in early development stages. Only a small number of project cancellations will severely impact Portugal’s ability to achieve its hydrogen production targets, underscoring the need for more project development to provide greater certainty to its production capacity pipeline.

Infrastructure gaps

Portugal aims to inject 10-15% hydrogen into its gas pipeline network by 2030, with a roadmap for full conversion finalised by the end of 2024. This initiative supports the country’s broader decarbonisation strategy, moving beyond isolate production projects.

Additionally, the converted network will be crucial for future exports through the H2Med project, linking the Iberian Peninsula to Northwest Europe. The pipeline is undergoing various engineering and financing studies, which are expected to finalise in 2025. This network will be part of the European Hydrogen Backbone, connecting Iberian renewable hydrogen to key import-dominant markets like Germany[5].

Due to continued uncertainty in network development, Iberian developers are exploring derivatives, such as ammonia, for nearer-term export opportunities to the Port of Rotterdam, contingent on the necessary port infrastructure in Iberia.

Key conclusions

Spain and Portugal are well-positioned to play a leading role in the European hydrogen market due to their advantaged renewable energy resources, but this alone is evidently not enough to surpass the rest of Europe.

Both countries face significant challenges in project development, funding and infrastructure that mirror those seen across the continent. While projects are generally aligned with existing industrial demand, progress has been hindered by delays in funding, a lack of offtake agreements and infrastructure gaps.

To truly capitalise on their advantages and grow necessary momentum, Spain and Portugal must accelerate government support, secure reliable infrastructure, and overcome the critical challenges preventing projects from reaching FID. This will be essential for both Iberia’s and the wider continent’s decarbonisation ambitions.

Jun Sasamura, Senior Analyst – Hydrogen

[email protected]

Ben Clark, Senior Analyst – Hydrogen & CCUS

[email protected]

Arthur James, Analyst – Hydrogen

[email protected]

[1] Draft update to Portugal National Energy and Climate Plan under public consultation until September 2024

[2] The EU REDII Delegated Act includes a clause stating that if the share of renewables in the electricity grid is greater than 90%, hydrogen projects will not have to build additional renewable energy capacity to supply it

[3] According to Westwood’s project certainty criteria

[4] The EU’s Renewable Energy Directive definition of renewable fuels of non-biological origin (RFNBO), which includes electrolytic hydrogen production from renewable electricity

[5] Germany expects 50%-70% of their project hydrogen demand by 2030 to be met by imports

Join Jun Sasamura and Arthur James on Thursday 19th September for a webinar that will further explore the themes presented in this Westwood Insight. Register here.