India continues to reign as the world’s third-largest energy consumer, and by 2030 the IEA forecasts gas demand of 103bcm per annum, up 60% on 2023 levels. Liquid demand is also trending upwards, with the Indian Energy Minister expecting the country to account for 25% of incremental global oil demand over the next two decades, a forecast that aligns with the EIA’s 2030 Indian liquid demand expectations of 6.6mmbpd, up 20% on 2023. That said, India continues to struggle to meet its hydrocarbon demand from domestic production, highlighted by the 3.7%[1] YoY increase in its crude import bill reflecting an 88.1% crude import dependency. These figures indicate a striking need to address the growing domestic hydrocarbon supply deficit – thus the Indian government announced a US$67bn investment budget to increase the share of gas production in the energy mix from the current 6.83%[2] to 15% by 2030. Despite these ambitions, the question remains around India’s true ability to absorb more of its domestic demand and meet its 2030 gas target, given its challenges with depleting production and limited large discoveries.

India aims to add 1 million sq km of exploration acreage by 2030, and since 2019 has launched 10 Open Acreage Licensing Policy (OALP) bidding rounds, offering a total of 144 exploration blocks. The latest offering is the 191,986 sq km OALP X bidding round launched in February 2025, covering 25 exploration blocks, 12 onshore and 13 offshore blocks. On the regulatory end, India’s parliament passed the Oilfields (Regulation and Development) Amendment Bill 2024 in March 2025. This bill replaces the Oilfields (Regulation and Development) Act 1948, bringing in key reforms to its oil and gas laws and introducing clauses that support smaller operators and new entrants.

Drilling outlook to 2030

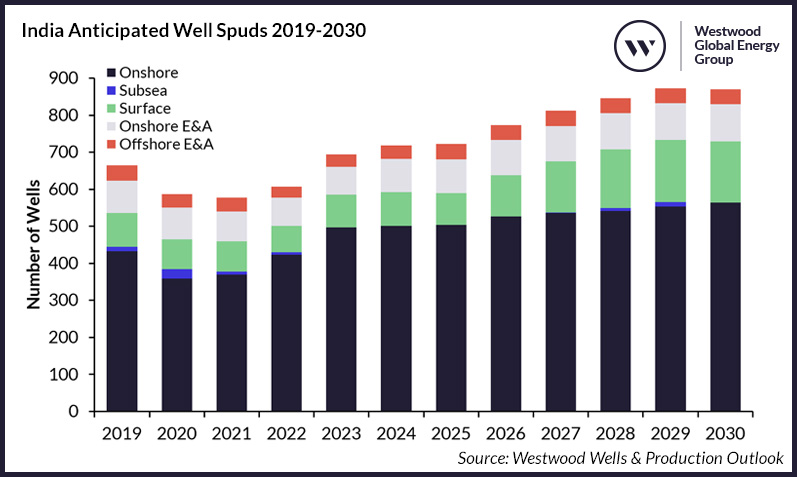

Between 2025 and 2030, an average of 811 wells are anticipated to be spud annually, onshore and offshore, up 21% on the five-year hindcast. Of these spuds, 78% will be onshore, driven by infill development drilling to arrest production declines at mature fields and to support brownfield expansions. Various domestic operators have indicated plans to augment infill drilling, with the most recent example being Cairn Oil & Gas, which is planning to invest US$3-4bn towards production growth in its Northeast assets and in the Mangala oilfield. Thus, over 3,000 development wells will be drilled onshore over the 2025-2030 period, up 22% on the hindcast. Onshore E&A drilling is also set to increase by 17%, with a total of 581 wells forecast to be spud by 2030. A key contributor to this activity level will be the progression of Oil India’s 15,000 sq km exploration campaign in the Mahanadi Basin.

India Anticipated Well Spuds 2019-2030. Source: Westwood Wells & Production Outlook

By the end of the forecast period, a total of 1,100 wells are anticipated to be drilled offshore India. 75% of these spuds will be surface wells (platform wells), peaking at 170 wells in 2029 in anticipation of a production start from greenfield projects such as ONGC’s Cluster IX/X. Westwood’s RigLogix forecasts stability in the jackup market with approximately 40 rigs operational between 2025 and 2027, including the four jackups re-tendered by ONGC in February 2025. Offshore exploration drilling will grow by 10% in the forecast, with 45 spuds anticipated annually to support 2030 gas production targets. Westwood’s Wildcat identifies the possibility of ONGC and Oil India spudding up to five high-impact wells offshore India in 2025. However, there are upside potentials for further E&A drilling offshore India depending on the outcomes of current exploration rounds and a strong likelihood of India launching additional OALP bidding rounds.

Production outlook to 2030

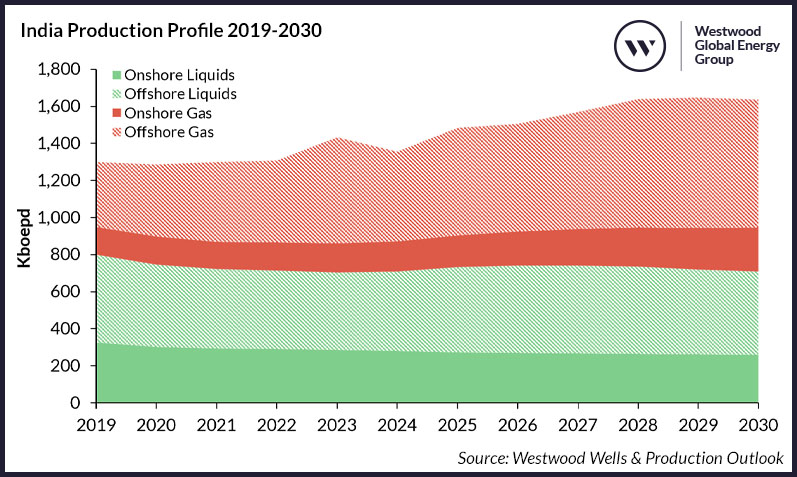

With this level of drilling activity, Westwood forecasts an uptick in overall oil and gas production to 1.6mmboepd by 2030, up 20% on the 1.4mmboepd produced in 2024. Gas will be the largest contributor, as production is anticipated to grow by 42% from 660kboepd (4bcfd) produced in 2024 to 940kboepd (6bcfd) in 2030. Gas output gains will be driven by shallow water projects, with key projects being ONGC’s Daman Expansion & Daman Upside projects, as well as ONGC’s Integrated Gas Development project, which could add a combined 152kboepd by the end of 2029. A significant gas output uplift is also anticipated, with BP appointed as the technical service provider for ONGC, which by 2028 aims to increase crude and gas output at the Mumbai High field by 44% and 89%, respectively, up from the 134kbpd of liquids produced in 2024.

Driven by these offshore projects, gas production from shallow water developments is anticipated to double to 500kboepd (3bcfd) by 2030, from the 250kboepd (1.5bcfd) produced in 2024. The crude production uplift from ONGC’s Mumbai High field as well as brownfield expansions in onshore terrains, such as Cairn’s 95kbpd Mangala field expansion project in 2025, will help stabilise liquids production at approximately 710kbpd by 2030, in line with 2024 output. However, Westwood cautions that should the liquids production uplift at ONGC’s Mumbai High field not materialise, India’s liquids forecast could be significantly diluted due to limited large discoveries and aggressive declines at mature fields.

India Production Profile 2019-2030. Source: Westwood Wells & Production Outlook

Despite India’s efforts to reduce its hydrocarbon deficit, current field development plans suggest that this is still a far-fetched reality. The launch of the OALP X bidding round, just six months after the OALP IX, highlights the government’s desire to take steps towards self-sufficiency. However, a lack of interest from non-incumbent companies and limited exploration success in recent years means that Westwood anticipates that this bidding round is unlikely to significantly uplift the country’s production fortunes. Therefore, it is highly probable that India will miss its 2030 target – to increase the share of gas production in its energy mix from 6.83% in 2024 to 15% – with it continuing to rank high among countries burdened by large hydrocarbon deficits.

Michela Francisco, Onshore Analyst

mfrancisco@westwoodenergy.com

A full in-depth country level overview can be found in Westwood’s Wells & Production Outlook 2025-2031. This is a series of four regional reports and accompanying databooks covering both onshore and offshore drilling and production outlooks for Africa & Europe, the Americas, Asia Pacific and the Middle East.