In a move that will create the largest international rig company by fleet size, Helmerich & Payne (H&P) has announced an all-cash, US$1.9725 billion deal to purchase KCA Deutag, with the acquisition expected to close by the end of the year.

While the news is still fresh, this agreement appears to be a good and complementary one for both businesses. H&P, which has one of the largest land drilling fleets in the USA (225 units), has slowly been increasing its international footprint. This move, part of an international growth strategy to diversify outside of its core US market, has been massively accelerated by the planned acquisition of KCA. Currently operating rigs in five different countries outside of North America (Argentina, Australia, Bahrain, Colombia and Saudi Arabia), the deal for KCA, a player with 129 rigs spread across 20 countries, immediately establishes H&P as a major player internationally as well as in North America.

This also helps to build up a strong backlog, which stands at US$5.5 billion for KCA (US$3 billion from land drilling), compared to US$1.7 billion for H&P. This highlights the different contracting strategies typical outside of the US, especially in the Middle East, where rigs are usually hired on multi-year contracts, compared to the short-cycle contracts that rule onshore in the US.

While the agreement may be for a global company with assets in multiple regions, the real prize is the boost it offers H&P’s presence in the Middle East and specifically the Gulf Cooperation Council (GCC) region. This was singled out by H&P’s CEO, John Lindsey, in a press release announcing the deal: “Acquiring KCA Deutag gives H&P immediate scale in core Middle East markets in a way that would be challenging to replicate organically.”

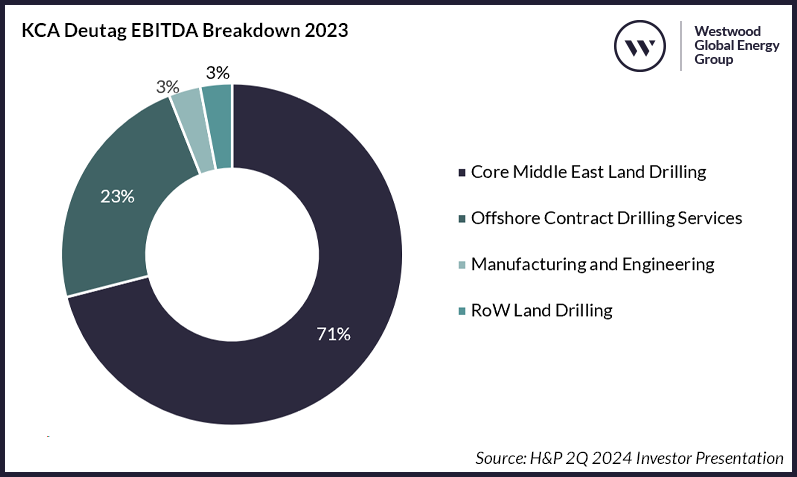

KCA is well established in the Middle East and 71% of the company’s EBITDA in 2023 came from land drilling operations in just three Middle Eastern countries – Saudi Arabia, Kuwait and Oman – termed as the “core countries”. In comparison, the rest of its land rig fleet (65 units across 17 countries) accounted for just 3%. These core countries that supported KCA’s strong EBITDA last year are also forecast to see major growth in the coming years.

KCA Deutag EBITDA Breakdown 2023

Source: H&P 2Q 2024 Investor Presentation

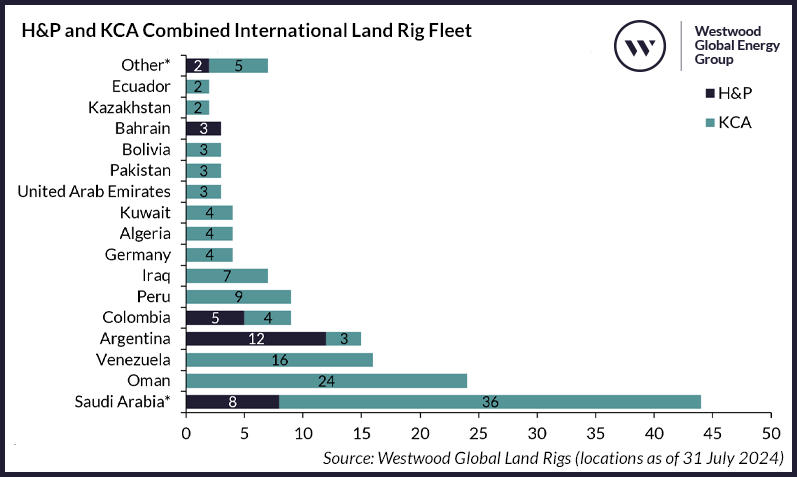

The combined company will now operate a fleet of 384 units (159 outside of H&P’s US rig fleet), placing them comfortably above the other major North American players such as Nabors, Precision Drilling and Ensign Energy and making H&P the largest non-NOC land rig company operating globally. The deal has limited synergies with a relatively small crossover in location between H&P’s and KCA’s existing fleets, and opens new areas, such as Europe’s geothermal drilling market, where H&P has no existing experience.

H&P and KCA Combined International Land Rig Fleet

Source: Westwood Global Land Rigs (locations as of 31 July 2024)

*H&P’s fleet includes eight rigs scheduled to move from the US to the Middle East, including seven to Saudi Arabia and one to an unidentified country (listed under other).

The acquisition puts the combined company in a great position to capitalise on the three core Middle Eastern countries, which are expected to see a 28% rise in rig demand by 2028. Westwood estimates that utilisation, which has hovered around 50% globally since 2022, reached 79% in 2023 in the three core countries and is expected to rise to 89% by 2028. This rise comes despite a raft of newbuild land rig additions to GCC fleets from major regional players, such as ADNOC Drilling, Arabian Drilling and the Saudi Aramco-Nabors JV SANAD.

Land Rig Utilisation and Wells Drilled in Core Countries

Source: Westwood World Land Drilling Rig Market Forecast

Saudi Arabia is undoubtedly a highlight for global rig demand over the forecast and is likely to be a key area for the combined company. For H&P, the Kingdom has been a recent success story. After a rig award was announced in August 2023, the company announced a tender award for a further seven rigs in February 2024, each with five-year terms and one-year options. All eight rigs have been sourced from H&P’s idle US rig fleet. Adding to this, KCA operates a fleet of 36 units within the Kingdom, announcing in April 2024 three short-term contract extensions worth US$16 million. By 2028, the strong level of utilisation currently seen in Saudi Arabia (88% in 2023) is forecast to reach close to 100%, likely offering further opportunities for H&P to move rigs from North America into the market.

Likewise, both Oman and Kuwait are areas where growth in drilling activity is anticipated over the forecast. While KCA is a relatively small part of Kuwait’s rig fleet (3%), it accounts for roughly 25% of the rig fleet in Oman, where close to 1,000 wells are expected to be spud annually through to 2028. In the same April 2024 announcement, KCA reported the award of a US$181 million contract for five rigs in Oman, equating to 18 years of work.

As ever, there are risks. The suspension of jackup contracts offshore Saudi Arabia shows that things can change very quickly, especially in a monopolistic contracting environment. However, the high number of wells forecast to be spudded (almost 10,000, 2024-2028), most of which are associated to already sanctioned projects, means this is unlikely to be an issue. But should activity levels drop significantly below our expectations, the picture could change.

One question raised by the transaction is whether it will inspire others to follow suit. While this is a possibility, especially for players looking to enter or expand their fleets in that lucrative GCC region, a deal of a similar scale is unlikely, given that much of the fleet within the GCC region is owned by state companies. While several of these are publicly listed, this is often just a percentage share of the business, making the full-scale purchase of a company with a similarly sized Middle Eastern rig fleet to KCA unlikely and, potentially, substantially more expensive.

Overall, the impending closure of the acquisition by the end of 2024 marks a significant milestone for the land rig industry. The merger of a company with a robust North American presence with another boasting a large geographical footprint, including a well-established presence in the high-demand GCC region, is expected to have a profound impact on the industry.

Ben Wilby, Senior Analyst – Onshore Energy Services

[email protected]

Featured data is sourced from Westwood’s Global Land Rigs and annual World Land Drilling Rig Market Forecast. For more information about our onshore energy market intelligence and commercial advisory services, please contact [email protected].