In view of attractive oil prices, an uptick in E&P investments and robust drilling activities, the active offshore support vessel (OSV) fleet increased by 22 vessels over the past 12 months and pushed effective utilisation to 75%. However, future utilisation remains contingent on fleet rejuvenation.

Robust 45% growth in offshore EPC investment

Oil prices sustained above $80/bbl since January as weaker demand fundamentals were offset by geopolitical risk in the Middle East and stagnant supply. Seasonal demand growth coupled with full OPEC+ cuts before the Group’s announcement to roll back on voluntary reduction from September should drive tightness in the global oil markets and maintain prices in the $80-90/bbl range; an attractive level to encourage investments into new projects.

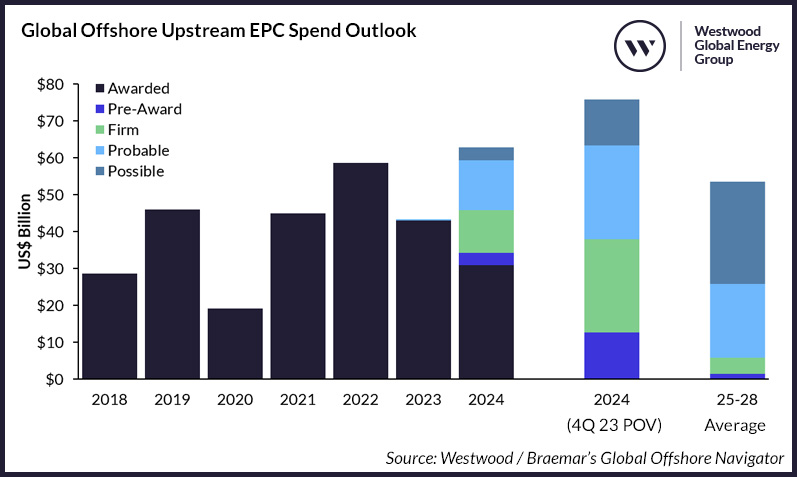

Upstream engineering, procurement, and construction (EPC) spend is projected to reach US$63bn for 2024, an annual uptick of 45% (see Figure 1). The top three spending regions for 2024 are Latin America (33%), Southeast Asia (14%) and the Middle East (12%). Middle Eastern offshore investment for 2024 is forecast at US$7.8bn, a dip of 49% after Saudi Aramco revoked its decision to increase production capacity to 13mmbpd by 2027.

Figure 1: Global Upstream O&G EPC Spend Outlook

Source: Westwood/Braemar’s Global Offshore Navigator

Global offshore drilling activities remained robust with contracted rigs standing at 526 units and marketed utilisation at 87%, the highest since 2016. Despite Saudi Aramco’s suspension of 22 jackups, effective utilisation sustained at 93% as affected rigs secured jobs outside the country, including Shelf Drilling’s jackup which moved to West Africa for drilling activities. Semisubmersible effective utilisation finished off the quarter at 83% and dayrates for new fixtures averaged nearly $400,000/day. Meanwhile, global drillship effective utilisation rounded off 2Q 2024 at 91%, with average fixture rate registering a YoY increase of 16% at nearly $480,000/day.

Influx of vessels to Latin America

In view of attractive oil prices, an uptick in E&P investments and robust drilling activities, the active OSV fleet rose to 3,125 units by end 2Q 2024. Over the past 12 months, an additional 22 vessels were added to the active fleet, the majority of which are platform supply vessels (PSVs). Latin America witnessed the most influx of vessels, largely attributed to inflow from the US. Meanwhile, active OSVs in Northwest Europe continue to fall as vessels were mobilised to Latin America, West Africa and the Mediterranean. A continuous flow of vessels into the Middle East region was observed, albeit less than the previous quarters. OSVs in Saudi Arabia were absorbed by EPCI contractors and moved to neighboring countries such as the UAE and Bahrain, a reversal of the situation from 4Q 2023. Southeast Asia expects to see more active vessels moving forward, with dayrates reaching comparable levels with the Middle East and increasing investment in deepwater oil and gas.

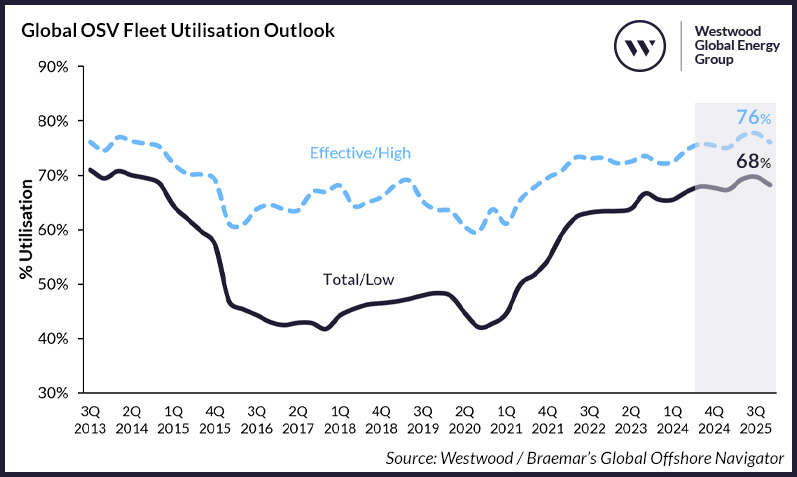

The laid-up fleet currently stands at 493 units, a YoY dip of 16% as vessels have been reactivated due to the increasing demand or conversions out of the offshore sector. Shrinkage of the OSV fleet coupled with an increasing active fleet have pushed global effective utilisation (excluding laid-up vessels) to 75% by end 2Q 2024. Future utilisation will be contingent on continued fleet rejuvenation, where Westwood expects utilisation to sustain at 75-78% over the next few quarters (see Figure 2). In the low-case outlook, which assumes no further scrapping, improving demand alone would increase utilisation to 71% by 2027. In the high-case outlook, utilisation could reach 80% should the entire laid-up fleet be removed from the market. A mid-case outlook on the other hand, assuming scrapping of the >15-year-old laid-up fleet, will result in 78% utilisation by 2027.

Figure 2: Global OSV Fleet Utilisation Outlook

Source: Westwood/Braemar’s Global Offshore Navigator

As highlighted in last year’s insight, global OSV supply is anticipated to tighten significantly over the next few years. Only 38% of vessels are in the Tier 1 category (likely to be delivered in the next 12 to 24 months), coupled with an additional 592 vessels becoming older than 15 years old and classed as non-premium.

Vessel owners react to ageing fleets

Rising inflation, stretched shipyard capacity to accommodate OSV builds, and difficulties in securing financing for newbuilds are hindering owners from pulling the trigger on placing new orders without the safety net of long-term charters in place. The sale and purchase market serves as an avenue for owners to boost their market presence against these challenges, with several large-scale transactions occurring in 2023 that saw key players expanding their fleet sizes, including Tidewater’s acquisition of Solstad’s PSV fleet and Britoil’s acquisition of OSVs.

Recent strategic movements that owners came up with to tackle the issue of ageing fleets while staying competitive in the market, include increasing investment to extend operational efficiency of vessels, greenifying assets’ engines to reduce emissions, or converting vessels to work in the renewables sector.

Nonetheless, there have been notable orders placed despite negative sentiments revolving around newbuilds. Owners have an alternative option of securing funding from capital management companies with favourable terms or coming up with capital to fund their own newbuilds. As seen by Capital Offshore, a new player set up by Capital Maritime & Trading that ordered four PSV newbuilds with four more letter of intents after acquiring seven PSVs from Standard Supply.

As the rate of scrapping and write-offs supersedes the rate of deliveries, tightening supply is likely to encourage fleet acquisition and upgrades to sustain competitiveness in the market while pressurising E&Ps to re-evaluate age restrictions for future operations.

Chen Wei, Senior Manager – Offshore Energy Services

[email protected]

Featured data is accurate as of 1H 2024 and is derived from the Global Offshore Navigator. Joint authored by leading experts from Braemar and Westwood, this quarterly market report provides informed data and analysis on key themes, drivers of demand and in-depth OSV market trends. For more information or purchase options, please click here or contact [email protected].