Political and fiscal uncertainty has undermined investor confidence in the UK oil and gas industry. Production is in decline, progression of new field developments has stalled, and exploration activity is at an all-time low. 22 fields ceased production in 2024 and 40% of fields that are currently producing or under development could cease economic production before 2030, based on current firm investment plans. A similar number could cease between 2030 and 2035. Decommissioning activity should be ramping up, because over the next 10 years more than US$26 billion could be spent on decommissioning in the UK.

Well plug and abandonment (P&A) activity accounts for approximately 50% of decommissioning spend, therefore the UK offshore drilling rig market would be expected to be in a buoyant state with a healthy backlog of work.

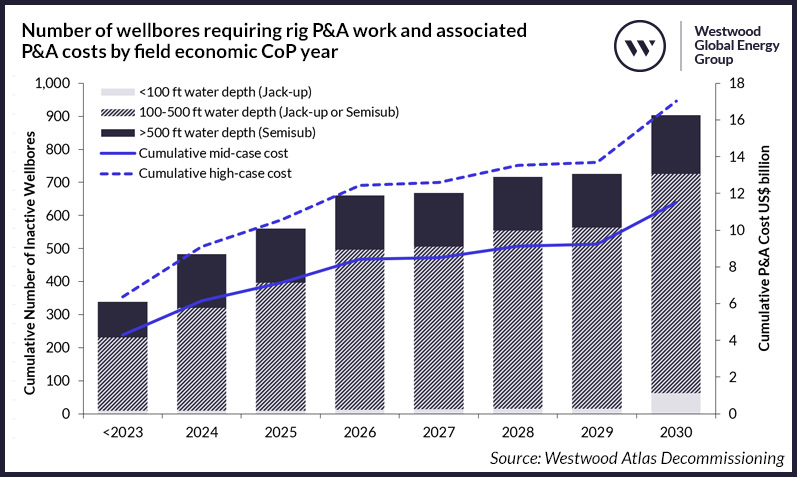

Westwood has evaluated the outstanding and future well P&A activities in relation to the cessation of production (CoP) year for fields, specifically for wells that require a semisubmersible or jackup unit for the activities (Figure 1). At the end of 2024, 483 wellbores require abandonment activities which will need drilling rigs. Assuming mid-case P&A durations, based on NSTA benchmarking, this equates to 70 years of P&A work. The NSTA guidance is for P&A activities to be completed within two years of CoP or a maximum of five, however, 73 of these wellbores have had well P&A work outstanding for more than 10 years.

Figure 1: Number of wellbores requiring rig P&A work and associated P&A costs by field economic CoP year. Note: Wells expected to use platform drilling facilities for P&A operations are excluded. Cumulative costs use the mid-case (P50) and high-case (P75) P&A costs from the NSTA’s UKCS Decommissioning Benchmarking Report 2024. Source: Westwood Atlas Decommissioning, NSTA.

Westwood estimates that by the end of 2030, a further 420 wellbores will be added to the abandonment pool requiring rigs, equivalent to another 61 years of activity. This level of demand should in theory sustain rig utilisation dayrates in the near to mid-term for both jackups and semisubs. But P&A execution rates to date are lagging behind demand. There are only a limited number of rig contracts being awarded for P&A work. Of the 22 rigs (eight semisubs and 14 jackups) currently based in the UK, four are carrying out P&A work and three are stacked (two semisubs and one jack-up). There is a real risk of rigs moving overseas for contracts or rigs being retired. This would constrain future supply capability to meet the inevitable P&A requirements, which would inevitably lead to an increase in rig dayrates and other supply chain costs.

The impact of increasing service sector costs could have a significant impact on future P&A expenditure. For the wells expected to become inactive by end 2030, Westwood estimates that up to US$5.5 billon could be added to well P&A costs through cost inflation or execution inefficiencies. With the impact of decommissioning tax liabilities on abandonment expenditure, cost-effective P&A must be paramount.

There is sufficient P&A workscope to keep rigs, and the associated services, busy through to the mid-2030s in the UK, but contract awards are not aligning with available work. The longer well P&A work is delayed, the more wells are added to the outstanding work, which increases pressure on the supply chain, particularly rig demand, leading to increased costs. If companies continue to defer P&A activity, the uncertainty for the supply chain increases and this could be detrimental to the effective delivery of decommissioning in the UK.

Yvonne Telford, Director – Northwest Europe E&P

[email protected]

Featured data and analysis is derived from Westwood’s new Atlas Decom, which is available now as a fully integrated module in the existing Atlas market intelligence solution, or as a standalone offering.

Read the press release announcement here.