Higher oil prices in 2021 led to a healthy rebound in global drilling activity the following year, helping production in areas such as the USA and Brazil reach new heights. Indications of a softening drilling market in certain areas were seen in 2023 but became more prominent in 2024 with lagging rig activity onshore USA and high-profile rig contract suspensions onshore and offshore Saudi Arabia. With OPEC+ agreeing on 5 December to extend its voluntary output cuts into 2025, there are indications that the market may shrink further as we enter 2025. Westwood’s latest Wells & Production Outlook indicates that, although there are undoubtedly some downward pressures for drilling, especially in the short-term, the global picture still has significant positives.

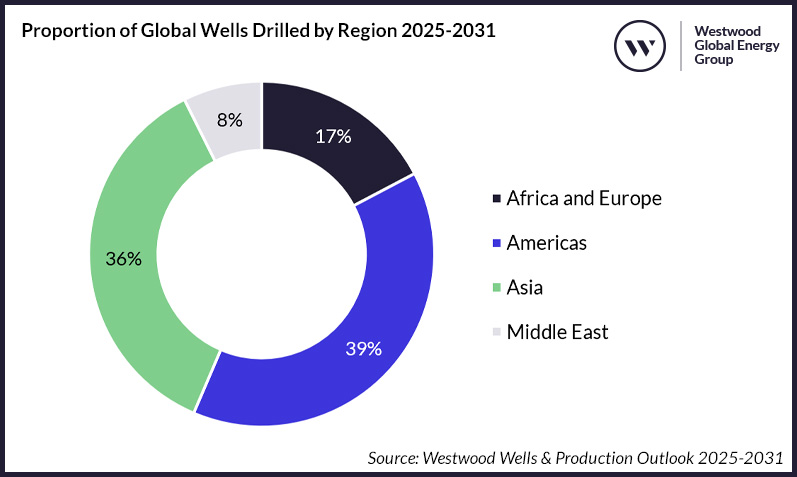

Over the 2025-2031 period, Westwood forecasts an average of 53,000 wells to be spud annually. On a regional level, the Americas is expected to lead drilling activity, driven by the USA (68% of regional activity), followed by Asia, where China dominates with 81%. Africa and Europe will be driven by activities in Russia, which will account for 79% of wells spud in the region, while drilling activities in the Middle East are more even spread, with the largest country, Oman, representing 27%.

Proportion of Global Wells Drilled by Region 2025-2031

Source: Westwood Wells & Production Outlook 2025-2031

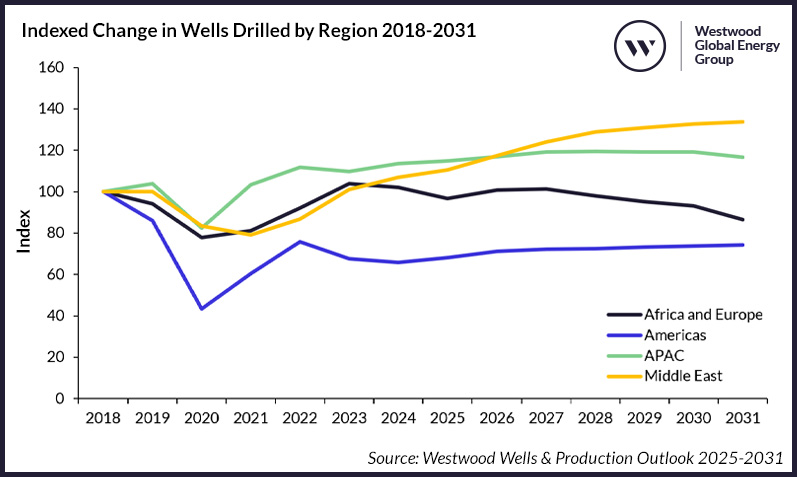

Back in 2018, the first year covered by this edition of the report, 59,000 wells were drilled globally. This is more than any year since, and any year expected over the forecast. Indexing this year to 100, it becomes clear that Asia and the Middle East are both expected to improve on 2018 levels throughout the forecast, with the number of wells drilled 18% and 26% higher over the forecast respectively. For Asia, this will be driven by China, which is expected to continue drilling >10,000 wells per year, while other countries, such as Indonesia and Thailand, drill at greater rates. The Middle East is expected to see the largest improvement, averaging over 4,000 wells per year, as NOCs ramp up drilling operations in onshore unconventional projects and brownfield offshore projects. Conversely, Africa and Europe, which are collated into one region for this report, are expected to average 9,360 wells over the forecast, down 4% on 2018.

Indexed Change in Wells Drilled by Region 2018-2031

Source: Westwood Wells & Production Outlook 2025-2031

The region that stands out most clearly however is the Americas – the largest driller but also the one with little to no forecast growth. Taking 2018, when 26,300 wells were drilled as 100, the average indexed rate of drilling over the forecast will be 72, with an average of 19,000 wells drilled per year. This compares to 95 (Africa and Europe), 118 (APAC) and 126 (Middle East).

Why is growth in the Americas so limited?

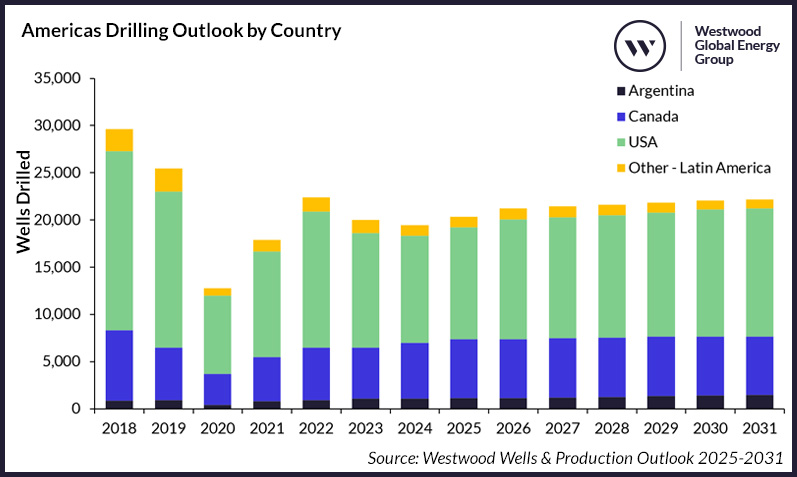

Regionally, North America (Canada and the USA) is expected to dominate, with drilling in the Lower 48 remaining the key driver of regional activity.

Americas Drilling Outlook by Country

Source: Westwood Wells & Production Outlook 2025-2031

However, the USA is not expected to return to previous drilling levels. Instead, the country is forecast to continue to be dominated by the theme of capital efficiency and profit over pure production growth. 2024, a year with low natural gas prices and high supply costs, has shown that if market conditions aren’t right, operators will not hesitate to reduce rig activity until market conditions improve. Drilling in 2024 is estimated to be 7% lower than 2023 and 40% below 2018.

Technological and drilling advancements are likely to be a major theme over the forecast, with operators drilling longer laterals and U-turn wells to further extract maximum value from each well. This is expected to continue to put downward pressure on the number of wells required annually, with an annual average of 12,400 onshore development wells over the forecast, 2% below an annual average of 12,700 wells in a hindcast impacted by the COVID-19 demand destruction in 2020.

The election of Donald Trump and his “drill baby drill” slogan is unlikely to receive much of a reaction from operators predicted to continue with their capital conscious approach. However, the expected rescinding of Biden’s pause on approvals of new LNG export agreements should support an uplift in drilling in the shale basins with a higher gas content, which has been hit particularly hard this year. Activity in the USA has settled into a new normal – with the previous levels of drilling highly unlikely to be seen again. For those service companies and rig contractors who can offer the technologies and rigs that are growing increasingly important to operators in the shale plays, there remains huge opportunities despite the reduction in the volume of wells drilled.

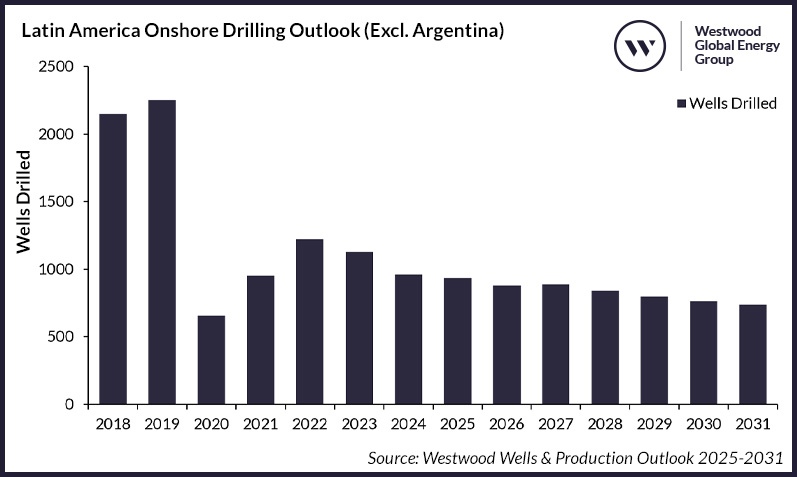

Another reason for the decline in drilling activities in the Americas since 2018 is onshore Latin America, where there is a limited positive outlook except for Argentina. The entire region is on a downward curve over the forecast as dwindling reserves, poor economic factors and political unrest impact drilling activity.

Latin America Onshore Drilling Outlook (Excl. Argentina)

Source: Westwood Wells & Production Outlook 2025-2031

In Mexico, 52 onshore wells were drilled in 1H 2024, compared to 88 in 1H 2023, a 41% decline YoY. This comes despite several promising condensate discoveries in recent years (Ixachi, Quesqui and Baktegas) and the delivery of 10 newbuild land rigs. It is unclear what impact the new president, Claudia Sheinbaum, will have on an industry that subsequent governments have failed to materially improve. However, Westwood does expect some improvement on the low 2024 figure (estimated at 85 for the year), with an average of 126 onshore wells over the forecast.

Other regional players, including Colombia and Peru, have consistently recorded drilling numbers below historic levels in recent years, and there is little indication of improvement. This is despite some bullish production forecasts and new schemes in most countries to raise production – something that has failed to translate into material production improvement in the past.

Bright spots

Despite this, there are several areas of the Americas predicted to see major growth over the forecast, including Argentina, where activity has ramped up from a low of 430 well spuds in 2020 to 1,071 in 2023. Operators pledged investments of US$9 billion into the Vaca Muerta shale play in 2024 and is on track to beat 2023 with 546 development wells drilled in 1H 2024, up 11% YoY. Removing restrictions on investment has become the centrepiece of the current government, given historic issues. This, coupled with increased offtake routes, should see the number of wells drilled increase YoY to almost 1,500 by 2031, a potentially conservative number but one reflective of the challenges that remain.

Argentina remains beset by economic problems, while any potential changes in the government could disrupt the industry as they have in the past. On a more practical level, a significant increase in both equipment, including onshore rigs, and export infrastructure is vital to ensuring that growth can be maintained.

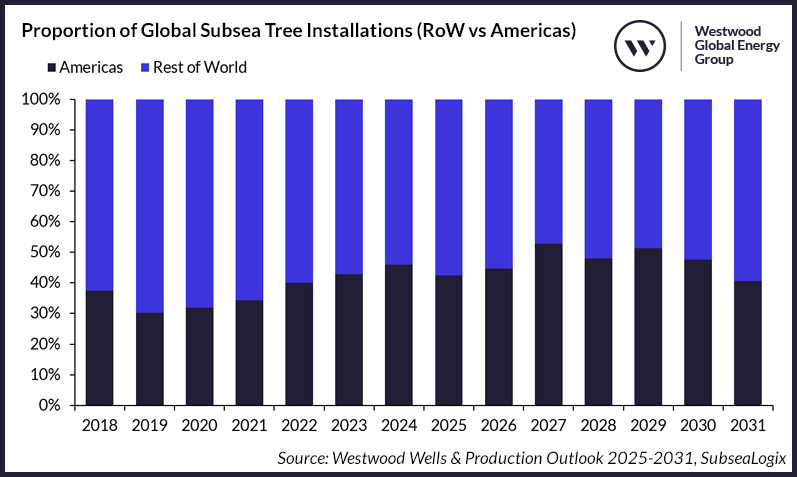

Another key bright spot is in the subsea sector, where the Americas is forecast to lead global demand for subsea development wells, accounting for 47% over the forecast period, a 37% increase on the hindcast. This reflects the increase in activity in the well-established Brazilian deepwater sector, which will lead subsea development with 360 wells spud. Guyana will also have an increase in activity, with 220 subsea development wells expected over the forecast. Furthermore, the recently sanctioned GranMorgu will kickstart an era of deepwater development drilling offshore Suriname. Petronas’ discoveries in Suriname’s Block 52, as well as Petrobras’ and Shell’s gas discoveries offshore Colombia, add further interest and upside potential in the buoyant deepwater region.

Proportion of Global Subsea Tree Installations (RoW vs Americas)

Source: Westwood Wells & Production Outlook 2025-2031, SubseaLogix

Continued strong investment in the deepwater US Gulf of Mexico will also boost regional activity, with approximately 115 subsea trees installed over the forecast. At the same time, the first deepwater fields in the Falkland Islands, Mexico and the aforementioned Suriname are expected online, adding a combined 84 subsea development wells to this already dominant region for subsea activity.

With more than 133,000 wells to be drilled over the forecast, the Americas continues to represent a major area for drilling. The region is expected to remain a bright spot for deepwater drilling, led by Brazil and Guyana, while onshore North America is expected to remain in high demand, albeit with activity in the Lower 48 settled into a new normal. Argentina is expected to be a bright spot in what is otherwise a more negative outlook onshore Latin America.

Ben Wilby, Research Manager – Onshore Energy Services

[email protected]

An in-depth country level overview of the fundamental drivers responsible can be found in Westwood’s Wells & Production Outlook 2025-2031. This is a series of four regional reports and Excel databooks covering both onshore and offshore drilling and production outlooks for Africa & Europe, the Americas, Asia Pacific and the Middle East.