4th December 2017

The eagerly-awaited outcome of the 173rd OPEC meeting (not to mention the third OPEC & non-OPEC ministerial meeting) was announced on 30th November. The summary headline is an extension of current cuts through to the end of 2018, with a cap on resurgent Libyan and Nigerian production and an agreement to review in June 2018. The reaction of oil industry professionals will no doubt have been a collective sigh of relief, as there is widespread recognition of the fragility of the present recovery and dependence on OPEC restrictions to support it. Using production and project data from Westwood Global Energy’s SECTORS online tool, we can evaluate the near-term impact of the cuts and also the potential longer-term outlook for supply and demand fundamentals, based on what is visible today.

OPEC has maintained an impressive discipline throughout 2017. For the ten members that agreed to reduce output, compliance has averaged at 107% overall this year to date, with countries such as Saudi Arabia cutting further than required. Saudi Arabia has much at stake; with a potential IPO of Saudi Aramco next year, there is every incentive to support oil prices (and therefore valuation).

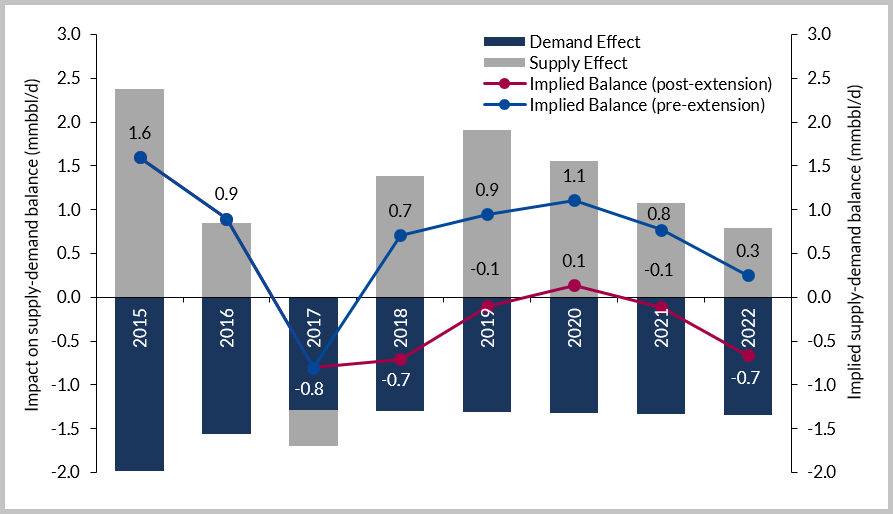

Thus far, the cuts have had the desired effect. Brent crude, at the time of writing, is $63/bbl, with WTI near $58/bbl. Substantial excess supply has been taken out of the market, mostly as a function of the OPEC cuts, but also due to steady erosion of excess supply from demand growth and natural production decline at existing fields. However, Westwood’s data shows substantial additional volumes coming to market in 2018 and 2019 as a result of new field developments commissioned prior to the downturn. Without the extension of the cuts (indicated by the blue line on the chart below) the market would have reverted to excess supply and potentially materially lower oil prices in 2018.

Magnitude of Supply Cut and Impact on Supply/Demand Balance

Magnitude of Supply Cut and Impact on Supply/Demand Balance

Source: Westwood Global Energy, SECTORS

The impact of the extended cuts (indicated in red above) takes the market into an undersupply situation, and will erode current stockpiles, which OPEC estimates in OECD countries at 140 mmbbl, at the rate of 0.7 mmbbl/d. This should support oil prices in 2018. Beyond 2018 the need for further extensions is evident by the projection of continued cuts at the same level (red line post 2018).

Beyond 2019 there remain uncertainties. Will the behavior of Saudi Arabia be the same if they successfully complete the Aramco IPO? Will OPEC remain disciplined? If the OPEC cuts come to an end in December next year, Westwood’s data suggests that the market will be oversupplied until next decade. OPEC members are clearly concerned about both higher oil prices bringing more US supply to market but also the impact of withdrawing the quota suddenly. With the quotas underpinning the current recovery, all eyes will nervously be on OPEC once more in June next year.

Matt Cook, Senior Analyst, Global OFS Research

[email protected] or +44 (0)1795 594735

Steve Robertson, Head of Global OFS Research

[email protected] or +44 (0)1795 594734