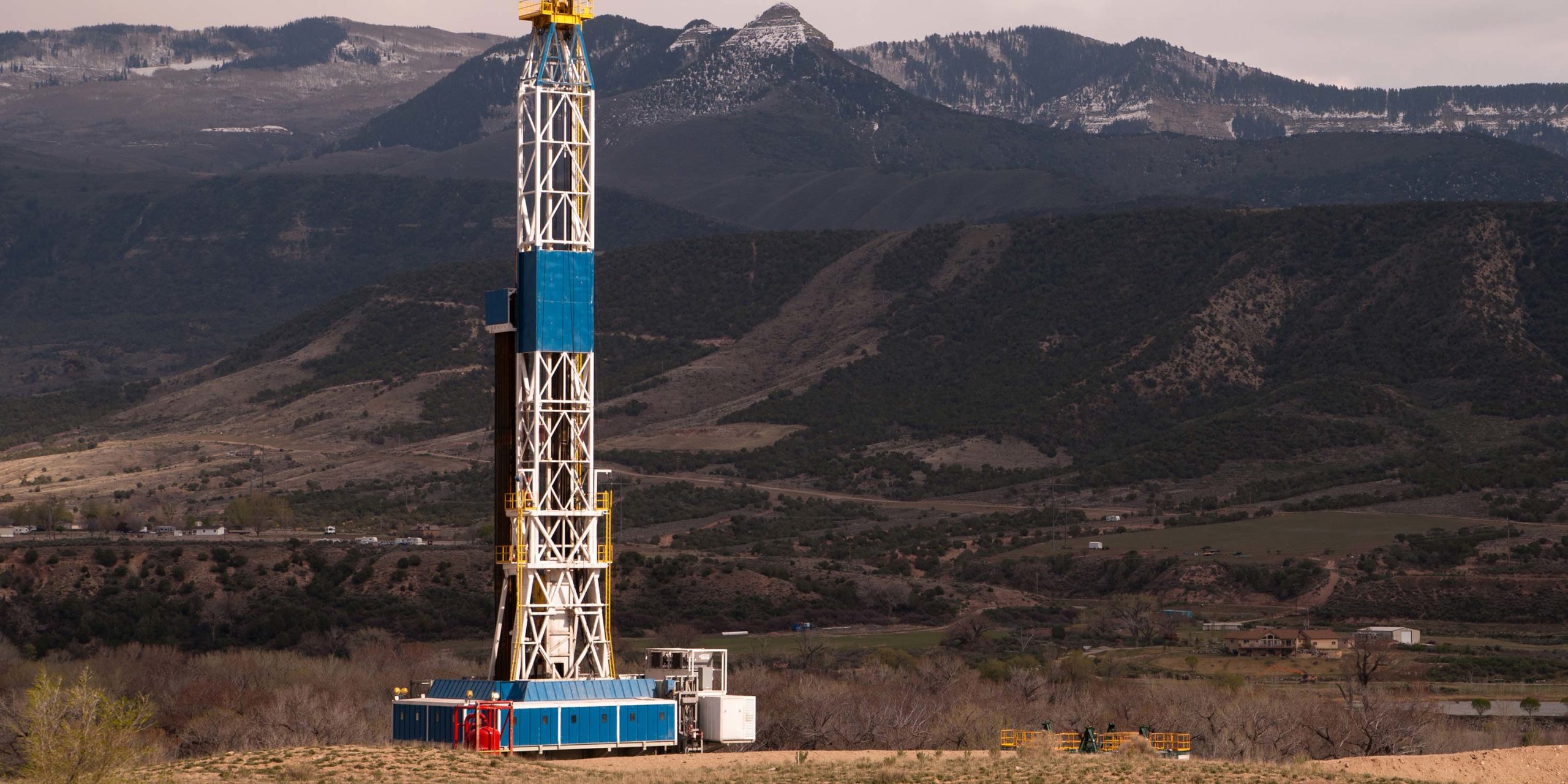

The global land drilling rig market has been through a tough downturn characterised by an inward focus through the supply chain on survival. This has had a considerable impact on the supply chain with a number of mergers, acquisitions and bankruptcies, in addition to aggressive measures for reducing operating costs.

The market has now turned and rig counts are climbing. Furthermore, the technical complexity of wells, particularly in North America, is changing at a dramatic rate. Only a few years ago the cost of the rig versus the completion for a North American well would have been 70:30 in favour of the rig – this has now flipped in favour of the completion, and operators are continuing to push the boundaries. Hess will reportedly conduct pilots for two new completion designs in 2017, one of which involves increasing the number of completion stages to 60 from the previous 50-stage design. The second pilot will involve testing the technical limitations in terms of proppant loading.

Following a 48% decline in 2016, the volume of onshore wells drilled in the US is expected to rise at a 11.2% CAGR through to 2023, constrained in the near-term by the speed at which rigs can be re-activated and crews hired. The move to longer laterals and more complex completions will favour higher-HP rigs that operate and move efficiently.

Internationally, rig operators have been consolidating their presence in markets where strong prospects for growth have been identified. Notably, in late 2016, Nabors and Saudi Aramco announced the signing of an onshore Joint Venture (JV), intended to own, manage, and operate land rigs in Saudi Arabia. According to data presented in Douglas-Westwood’s Sector’s online service, total onshore oil & gas production in the Kingdom is expected to increase steadily by 6.8% over 2017-2023, and the Nabors-Saudi Aramco JV highlights the aim of the world’s largest onshore rig contractor to cement its portfolio in the country.

More recently, in January 2017, Italy’s Saipem announced that it has been awarded an extension of pre-existing contracts for onshore drilling and workover work in MENA (Saudi Arabia and Morocco), as well as the award of new contacts in Latin America (Bolivia and Argentina), consolidating its existing presence in these regions.

In some markets, contractors have been able to find work for their units outside of the oil & gas sector. Notably, in Indonesia, a rise in geothermal activity has meant demand for higher specification units (above 1000HP) has been sustained, despite rig day rates having been significantly reduced by the oil price downturn.

The pressure to reduce operating costs has also impacted the supply chain for rig equipment, in that there is an increased tendency for contractors to opt for spare components available from other rigs in the fleet or on the second-hand market, as opposed to purchasing directly from the Original Equipment Manufacturer (OEM).

The recovery and the increasingly-technical complexity of onshore wells will be a key trend in the coming years. The condition of the fleet of cold stacked rigs versus the cost of new, and potentially more efficient and competitive, rigs will be an important theme for the OEMs. Some rig contractors may opt for new equipment rather than reactivating rigs in poor condition, triggering a recovery also for equipment vendors.

Katy Smith, Researcher, Douglas-Westwood

[email protected] or +44 (0)1795 594745