6th November 2017

The analysis below is based on the income statements of 22 mid-cap international E&P companies between 2014 and 2017 H1. Key findings are as follows:

- Unit costs were reduced in 2017 H1, but the pace of unit cost cutting continues to slow.

- 2017 H1 was the first of the time periods studied where the impairment/boe cost was not the highest unit cost on the companies’ combined income statement.

- The weighted average Brent breakeven oil price (the price at which the 22 companies would breakeven on a pre-tax net income basis) is down from $64/bbl in 2014 to $40/bbl in 2017 H1 (-37%).

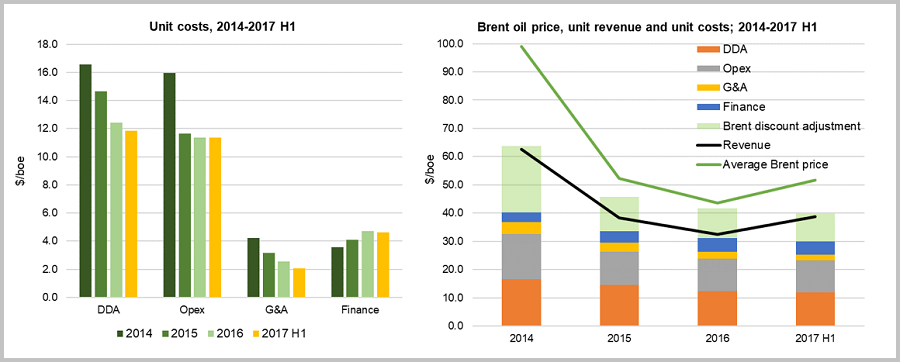

The table shows the combined mmboe production across the 22 companies and their overall $/boe metrics for each period, along with the average Brent price, the Brent discount in the companies’ revenue, and the resultant implied Brent breakeven price. This data is then depicted graphically to show year-on-year trends.

The overall unit cost base (comprising Opex, G&A, DDA, and finance) has declined from $40/boe in 2014 to $30/boe in 2017 H1; a decrease of 26%. However, the reductions in the cost base have progressively diminished. The impairment-driven DDA unit cost reductions account for 45% of the $10/boe decrease, and Opex savings account for 44%. 2017 H1 was the first of the time periods studied where the impairment/boe cost was not the highest unit cost.

Over the same period, the realised revenue/boe has tracked the Brent oil price, however, the discount to Brent has reduced from 37% in 2014 to 25% in 2017 H1. This is probably due to the presence of some gas pricing contracts not linked to oil prices. The combined effect of both the cost base reduction and the Brent discount reduction has meant that the decrease in the effective Brent breakeven price for the 22 companies has been much more pronounced, falling nearly $24/bbl (-37%) from $64/bbl in 2014 to $40/bbl in 2017 H1.

Following a 27% reduction in overall Opex/boe between 2014 and 2015, Opex/boe has remained essentially unchanged since then. Easier cost savings were quickly achieved following the oil price downturn, but further savings have proven more difficult to achieve. DDA/boe costs have reduced by 28% since 2014, but this is partly driven by cumulative impairments of $27.3bn over the time period. It is therefore hard to tell how much of these cost savings are structural, and will be applied in the longer term, as opposed to being impairment-driven (for DDA) or market-driven (for Opex). If oil prices continue to rise, will unit cost bases simply follow suit?

This is an extract from a longer article published in WGE’s Wildcat Corporate Monthly Report October 2017.

Robert Stevens, Analyst, Global E&A

[email protected] or +44 (0)20 3794 5378