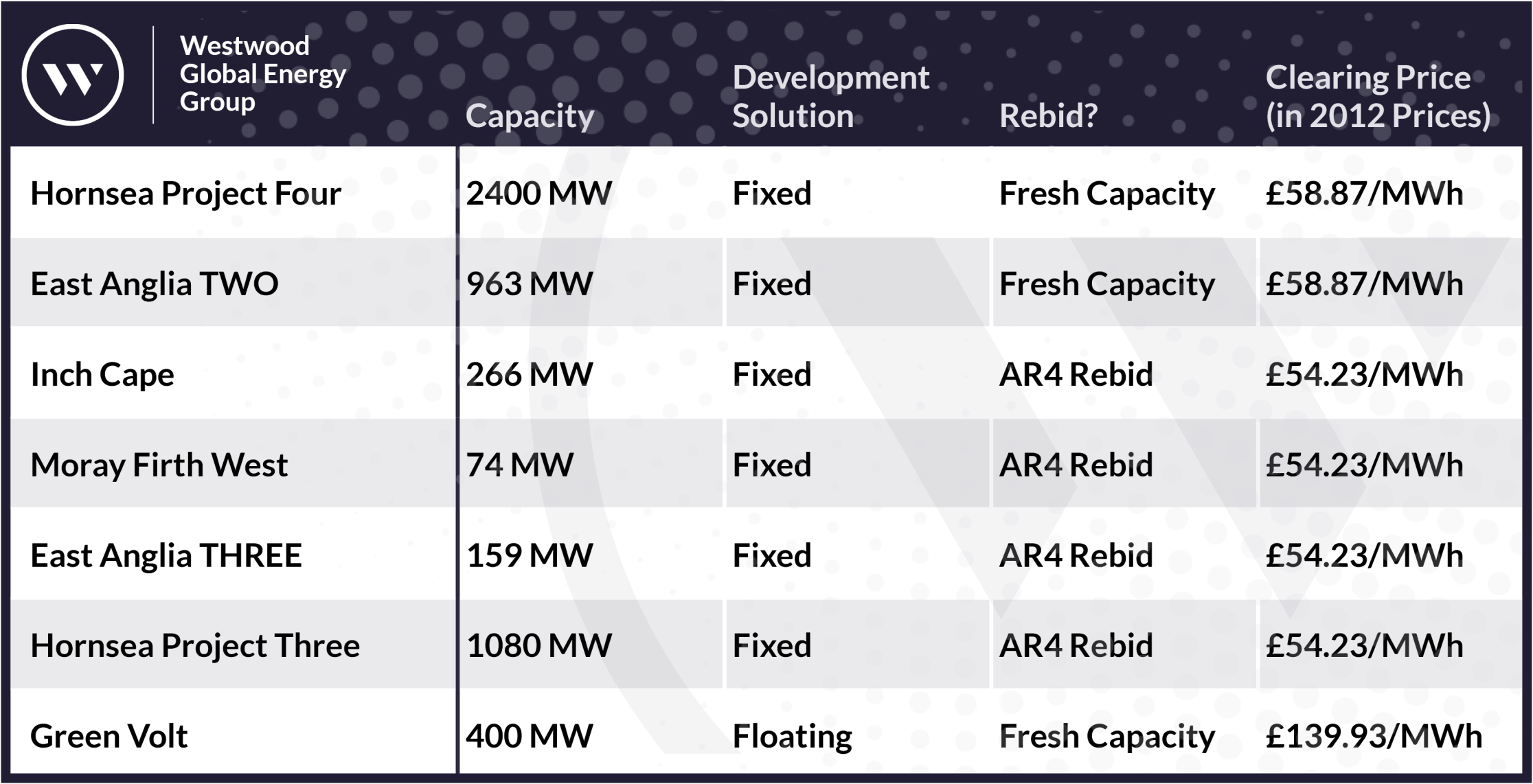

The UK government announced the results of the sixth Allocation Round (AR6) of its Contract for Difference (CfD) scheme on Tuesday. In total, 5.3GW of offshore wind capacity was a CfD in AR6, with 4.9GW of fixed wind contracted at clearing prices of £54.23/MWh and £58.87/MWh and 0.4GW of floating wind contract at £139.93/MWh (all in 2012 prices).

Source: Westwood WindLogix

AR6 was a mixed bag for offshore wind. While the headline award of 5.3GW is a huge improvement on the failure to award any capacity that was AR5, 1.6GW of that came in the form of rebids from AR4, clearing at a 45% increase in price to the original award. This restores some momentum to the sector, but still leaves the pressure on to reach 2030 targets. Interestingly, the highest clearing price for offshore wind in this round was £58.87/MWh, ‘only’ 34% higher than the much-lamented strike price in AR5 and someway below the maximum of £73.00/MWh set by the government for AR6, which only serves to highlight the extent to which AR5 was a lost opportunity (all at 2012 prices).

On the floating side, the award of a CfD to Green Volt continues a remarkable journey for a project that only received a lease in 2023 as part of the INTOG leasing process. However, the fact that one project was awarded all of the floating allocation in this round (edging out a number of demonstrators in the process) does inevitably increase the UK supply chain’s exposure to whatever foundation concept Flotation Energy selects for the site. Meanwhile, the £139.93/MWh at which it was awarded (in 2012 prices, closer to £195/MWh in today’s prices) will be a key point of comparison for floating projects going forward. The floating French project Pennavel secured subsidised offtake earlier this year at EUR 86.45/MWh (roughly £52.22/MWh in comparable CfD 2012 pricing), while the TwinHub Demonstrator picked up a CfD in AR4 at £87.30/MWh (in 2012 prices, about £121.60 in today’s prices), albeit with very unique site conditions. A fascinating spread in offtake prices for floating wind is thus emerging.

AR6 itself had something of an interesting life. The round opened in March 2024 under the then Conservative government and was notable for both ringfencing funds for fixed offshore wind in ‘Pot 3’ and significantly increasing the administrative price for the technology (the maximum bid price that could be offered by a developer) by 66% to £73.00/MWh (in 2012 prices).

After the round opened, however, industry concern migrated from the administrative price to the budget allocated. In particular, there were concerns that insufficient budget was being made available for the UK to meet its 2030 offshore wind goals and that assumptions about future electricity prices (which effectively set the limit on the amount of capacity that can be awarder) were too low. Given that only 3.3GW of new capacity was successful in AR6, competing as it had to with rebidding AR4 projects, these concerns do not appear to have been unfounded.

July 2024, however, saw a general election in the UK, with the Labour party forming a government for the first time since 2010. Following the change in government, lobbying efforts from industry to increase the offshore wind budget allocation intensified. The end result was an increase of £300mn in the budget for offshore wind, announced on the final day possible, with other technologies also seeing additional funds allocated.

All in all, the results of AR6 point to the growing complexity of the UK’s offshore wind market. The introduction of the yearly auction cycle (alongside the ability to rebid a portion of previously awarded capacity with limited penalty) has created complex bidding dynamics for developers, especially as market conditions remain volatile. Indeed, some upcoming projects will utilise multiple CfDs (set at different strike prices), CPPAs and the merchant market.

Further changes to the CfD regime may also be on the horizon, with the government having recently consulted on possible amendments for AR7. At the same time, there is the possibility of the introduction of CfD Sustainable Industry Rewards (‘SIRs’), which would see developers topping up their strike price by committing to investment in the supply chain. In any case, the CfD regime will have to be ready for the multiple gigawatts of floating wind projects now under development and likely to be seeking offtake in the next few years. Special measures, such as ringfenced funding, may have to be considered to ensure that the emerging industry is able to make progress in the competitive process.

After AR6 then, the future of offshore wind in the UK is at once a little clearer and more complex than ever.

Peter Lloyd-Williams, Senior Analyst – Offshore Wind

[email protected]