Momentum Returning to Rig Market Utilization – Are Dayrates Far Behind?

With the global offshore rig market starting to show signs of picking up, there has been a great deal written about the offshore rig recovery, and while rig owners in a few regions are enjoying high utilization and the dayrate benefits that go along with that, the same cannot be said for the fleet as a whole. Nevertheless, utilization for jackups, semisubmersibles (semis) and drillships has increased in 2019, with most key indicators pointing to a continued increase. Higher dayrates always follow improving utilization, and while there have been a few notable fixtures, how long will the gap be this time?

Westwood Global Energy has invested in developing a new set of rig market analytical tools, rebuilding the RigLogix platform to deliver enhanced functionality and insights.

Source: RigLogix

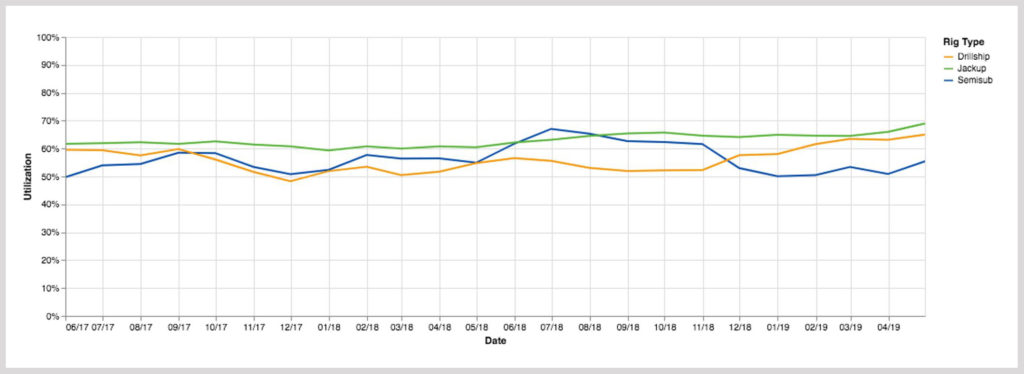

The New RigLogix dashboard shows a material utilization recovery for jackups and drillships over the last 12 months. Drillships have seen marketed utilization increase from 55% in May 2018 to 65% today, while overall marketed jackup utilization is now nudging 70%, also up nearly 10% from one year ago.

Although the utilization improvement displayed above has led to some selected dayrate increases, it generally takes 85-90% utilization before dayrates begin to accelerate at a faster pace, and there is still a ways to go to reach that level. In addition, there is always a lag period between utilization increasing and dayrates following suit. However, after an extended downturn with both utilization and dayrates at bottom-of-cycle lows, the market is watching utilization and new fixture rates closely to see when the improving utilization will begin to yield higher dayrates for the fleet as a whole.

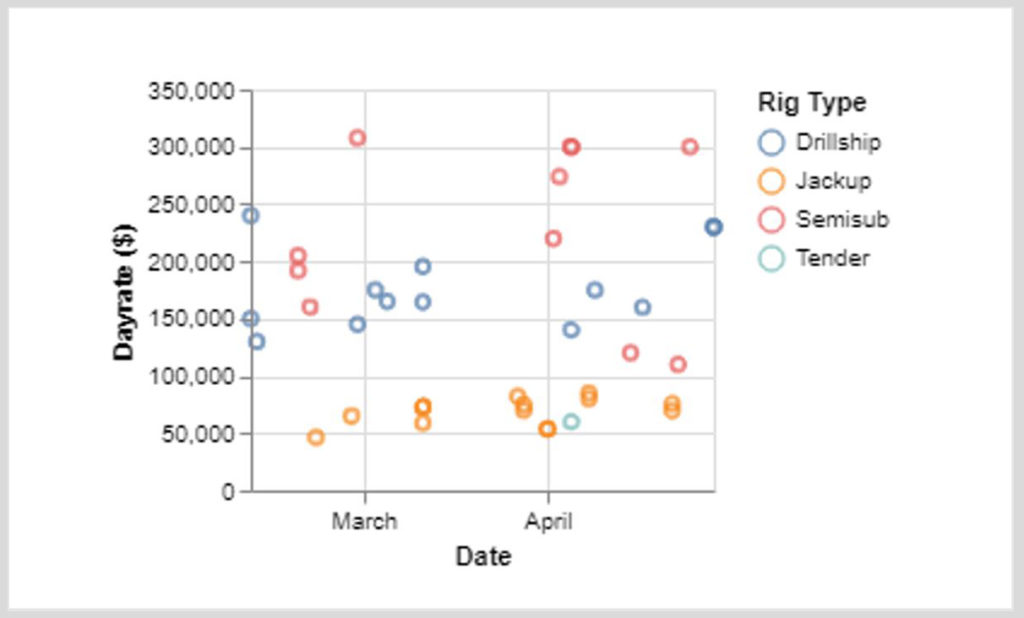

As seen in Figure 2, data from the New RigLogix shows that new contract fixtures for jackups, semis and drillships have so far in 2019 generally trended up, although not every fixture has been an increase over the previous level. Nevertheless, some regions have reached the 85-90% utilization level previously mentioned, and as a result, there are some interesting regional themes emerging.

Source: RigLogix

The Southeast Asia jackup fleet can be called a tale of three markets, at least as it pertains to day rates. A few recent contract signings have been at $80,000 or more, and reports are that some international rig owners are routinely bidding new work at or above that level. Meanwhile, indigenous rig owners, especially in Vietnam and Malaysia, are now getting rates in the $69-75,000 range. Finally, some other rig owners have continued to secure work at rates of $50,000 or less, where rates have been the past few years.

In looking at the fleet, RigLogix shows that best case marketed utilization is 76%. There are nine cold-stacked jackups and five others that will be leaving the area shortly, removing them from marketed consideration. Of the remaining 10 warm-stacked jackups in the region, none are said to be ready for work without 30-60 days or more of shipyard time. More importantly, nine of the 10 also fall out of favor with operators as they either have no work history (newbuilds) or have been idle for more than six months, two rig no-no’s specified by the majority of rig requirements in the area. While 76% utilization is a substantial improvement for the region, it is well below the level needed to spur day rate increases. However, with the rig specifics imposed by operators, there are virtually no available jackups; hence rates have risen despite the 10 idle units. Although some operators are said to be now relaxing these requirements, it has so far not made much of an impact.

In looking at jackup requirements in the region, RigLogix data shows there are 40-50 drilling programs ranging in status from an expression of interest to ongoing tender and ranging in duration to a single well to over a year, so there is clearly plenty of work for the fleet. Whether rig owners decide to mobilize rigs to the region – that can satisfy work requirements – remains to be seen, but either way this is a market to keep an eye on.

For floating rigs, outside the Norway the harsh-environment semi market, the rig segment getting the most attention is the ultra-deepwater (UDW) floating rig fleet, UDW defined as units rated to work in 7,500-ft or more. As of May 1, utilization of this fleet stood at just 63.3%, with 107 of 169 units either working or committed to future contracts. Utilization of the marketed fleet, which totals 139, is substantially higher at 76.9%. Many in the industry view the latter percentage as the true barometer of the market since cold-stacked rigs are not usually marketed. However, with the advent of what rig owners call “smart-stacked” or “preservation-stacked”, the time required to get those rigs back into service is considerably shorter. In addition, as seen in recent Petrobras rig tenders in Brazil, three cold-stacked units in the U.S. Gulf of Mexico were bid for work, so the automatic exclusion of these units in not always a given.

As detailed in RigLogix, a number of notable floating rig contract signings have been made in recent months for work in several regions. Operators in the so-called Golden Triangle, that is the U.S. Gulf of Mexico, South America (not just Brazil) and off the west coast of Africa have chartered rigs, with a few at new market-high day rates well over $200,000, good news for rig owners. However, a few of these come with asterisks as they include add-ons for integrated services or managed-pressure drilling (MPD) operations, to name a few, leaving the “clean” rate somewhat lower, Second, most of these newly-awarded contracts will not begin until the second-half of 2020 or later, and generally rates for contracts with a start date over a year away will be higher. Nevertheless, the fact that some operators are committing to a rig that far in advance is a clear sign that they can see the writing on the wall and are looking to sign up rigs in a lower rate environment.

We previously noted there were 107 UDW floating rigs working/committed. According to RigLogix data, 35 of the 107 (33%) are contracted into 2021 or later. Another 56 have contract end dates within the next year, but RigLogix identifies 14 of those have options that will likely be exercised and will keep them working for the remainder of 2020.

RigLogix clients are keen on identifying future opportunities using the ‘Rig Tenders’ function in the tool. Rig owners sometimes will try to strategically position their fleets in areas they believe the future hot spots are and where they have the best chance of securing work. Many times, a rig owner might take a lower day rate for contract in a particular region with the hopes of securing additional work once it is there. Stacking locations are not chosen lightly either. For instance, Las Palmas, off the Canary Islands, has become a major rig stacking area in recent years, not only due to its benign climate, which is said to have less of a detrimental impact on the rig, but it also provides quick and easy access to several different regions.

Looking ahead, RigLogix’s Rig Tender data shows that there are currently some 199 drilling programs planned worldwide over the next 3-4 years that designate either a semi or drillship to be used. Of course, not all of these will require a UDW floater, nor will all of them end up being drilled, but there will also be new plans added, so on the surface there should be enough work to increase UDW rig usage in the coming few years. Regionally, the Norwegian North Sea harsh-environment semi market has garnered a good bit of press the past year and deservedly so. Utilization is high and day rate fixtures have consistently risen, with several of the most recent contracts signed at or above $300,000. Currently, there are around 85 drilling plans for floating rigs in the region, and while not all of the drilling is not in UDW waters, the use of those rigs has increased in recent months. Africa is another region where we believe rig demand will increase over the next few years. Currently operators have 88 drilling plans for that area, including the west, south and east coasts. The Asia-Pacific area – Southeast Asia, Australia and the Far East currently tout 95 drilling plans for floating rigs. Finally, Central and South America, from Mexico down the coast of South America, has 56 floating rig drilling plans at the moment. In all of these regions, several discoveries have been made in recent months, and that has in some instances spurred other operators holding nearby acreage, in some cases in different countries, to accelerate their plans.

The New RigLogix platform now embeds a forecasting tool, RigOutlook, into the product, with the user able to interact and manipulate key assumptions such as rig retirement rate and macroeconomic/oil price outlooks. Forecasts are generated for rig supply and demand, utilization, and day-rates. The base-case suggests that by 2020 fixture rates will have improved materially and rates for units on contract will follow suit, albeit with the usual lag reflecting the time between fixture and starting contract. By 2021 we expect to see dayrates for rigs operating increase by at least 15%.

With so many idle units in the current market, rig owners have not hesitated to bid rigs from other regions if they believe it fits the criteria for the requirement, and many recent contract awards have borne this out. There have been contracts awarded for work off Senegal to rigs currently in the U.S. Gulf of Mexico, in the Mexican Gulf to a newbuild rig in China and in Brazil to two rigs that were both idle in Greece. Generally, an operator will look first to rigs already located in the region where the work is taking place, but with some rig owners willing to absorb mobilization costs and/or make concessions perhaps normally not made, that will sometimes make the difference.

Terry Childs, Head of RigLogix

[email protected]

In Houston on 16th May? Joint the RigLogix team for our launch events! Just click on the banner below to register.