Offshore Energy Data Dashboard

Each month Westwood’s Offshore and New Energies teams provide a global data update on oil and gas-related engineering, procurement and construction (EPC) awards, wind turbine generator (WTG) awards, and drilling rig fleet utilisation and contract backlogs for jackups, semi-submersibles and drillships. Offshore field development data is sourced from and analysed using PlatformLogix, offshore wind data is from WindLogix, and offshore drilling rig data is from RigLogix. Bookmark this page for regular updates on the health of the offshore energy and renewable sectors.

Offshore Field Development

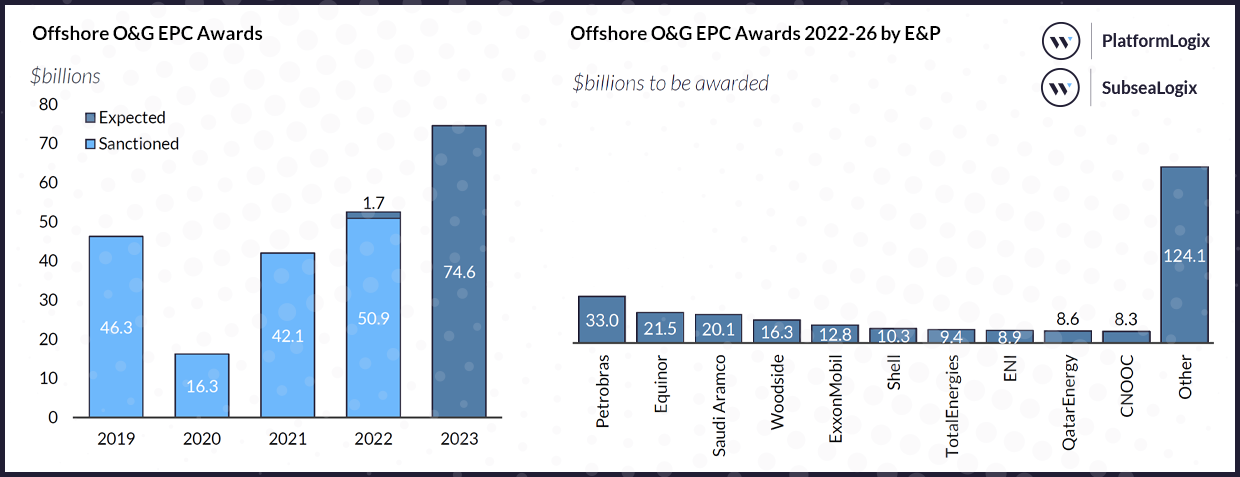

Offshore O&G-related engineering, procurement, and construction (EPC) contract award value in the last 30 days was estimated at approximately US$10 billion, bringing the year-to-date total to US$50.9 billion (excluding letters of intent). EPC award value in December has been predominantly driven by a wave of plans for development and operations (PDOs) submitted by Aker BP to the Norwegian Ministry of Petroleum and Energy for a total of 11 fields grouped into four main areas, namely Yggdrasil (formerly NOAKA), Valhall PWP – Fenris (formerly King Lear), Skarv satellite, and the Utsira High project. The PDO submissions also coincide with formal contract awards to Aibel, Aker Solutions, NZT, Siemens Energy and Subsea7 for the execution of various work scopes, including the engineering, procurement, construction and installation (EPCI) of fixed platforms, subsea production systems, line pipes and subsea umbilicals. Other key contract awards announced during the period under review include the transportation, installation and pre-commissioning of 170km of umbilicals awarded to Saipem for Eni’s Zohr gas field offshore Egypt, as well as the contract confirmation by the Subsea Integration Alliance for the development of BP’s Cypre gas project offshore Trinidad and Tobago.

Overall, Westwood anticipates 2022 offshore O&G-related EPC contract value to close at approximately US$53 billion, a 29% downward revision compared to our January 2022 outlook, as the year has been beset with major project delays and cancellations. Subsea tree order intake is set to close at over 280 units, whilst EPC-related activities fixed platforms and floating production systems sanctioned in 2022 are expected to close at approximately 100 units and 15 units respectively.

Looking forward, Westwood forecasts US$75 billion in offshore EPC contract award value for 2022, with Latin America, the Middle East and West Africa expected to drive contracting activities. Key projects to watch include ExxonMobil’s Uaru development (Guyana), ENI’s Baleine project (Ivory Coast), Woodside’s Trion (Mexico) and QatarEnergy’s North Field Sustainability expansion project.

Offshore Wind

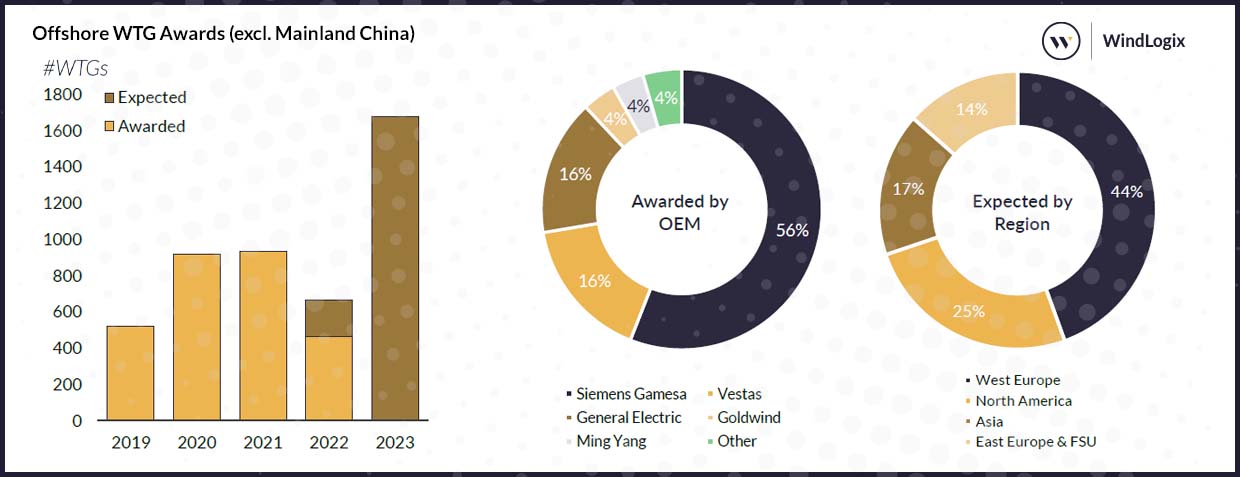

Since the last update, Vestas has been selected as the preferred turbine supplier for the MunmuBaram floating wind project, located offshore South Korea. The turbine OEM will supply and install 84 units of the V236-15.0 MW turbine and it will also deliver 20-year service and maintenance for the wind farm. The MunmuBaram project is being by developed Shell and Hexicon AB and will be constructed in three phases.

Dominating headlines was news that the provisional winners of California’s first offshore wind leasing round were selected via a competitive auction round. A total of five lease areas, which will host at least 4.6GW of floating offshore wind projects were awarded. The winning bidders were RWE Renewables, California North Floating, LLC (SPV of Copenhagen Infrastructure Partners), Equinor, Central California Offshore Wind LLC (50:50 JV of Ocean Winds and Canada Pension Plan Investment Board) and Invenergy.

Finally in the UK, Crown Estate Scotland announced that a total of 19 applications have been submitted for the Innovation and Targeted Oil and Gas (INTOG) offshore wind leasing round. A total of 10 applications have been submitted for the Innovation component and nine applications have been submitted for the Targeted Oil and Gas portion. Crown Estate Scotland is aiming to offer Exclusivity Agreements to the successful applicates by the end of April 2023.

Offshore Drilling Rigs

| Contract Backlog Month-on-Month (Rig Years) | Jackups | Semisubs | Drillships |

| November 2022 | 774.1 | 95.1 | 132.0 |

| December 2022 | 437.3 | 37.7 | 83.8 |

| Difference | -336.7 | -57.4 | -48.2 |

*Correct as of 20th December 2022

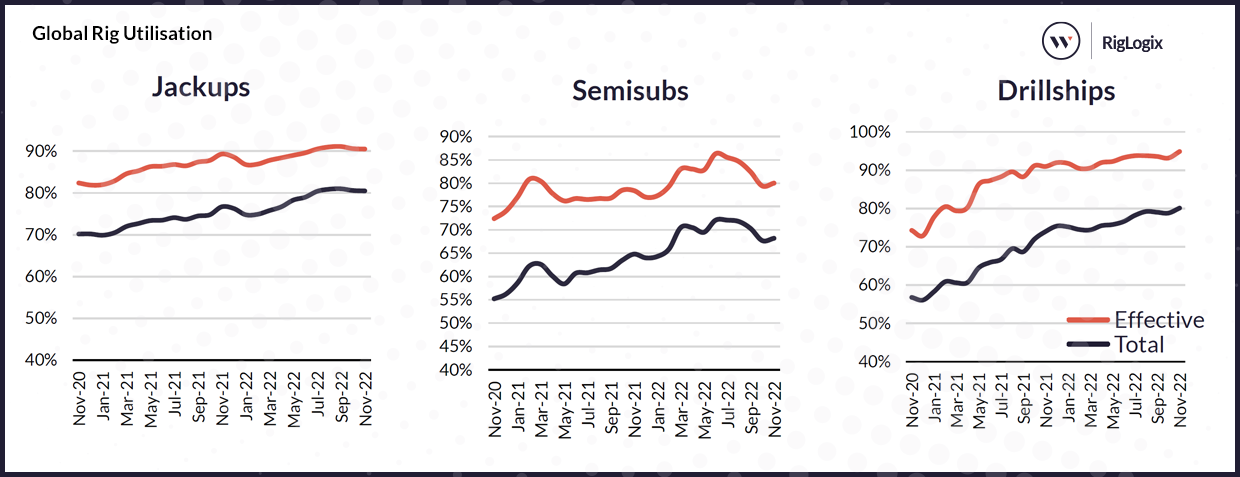

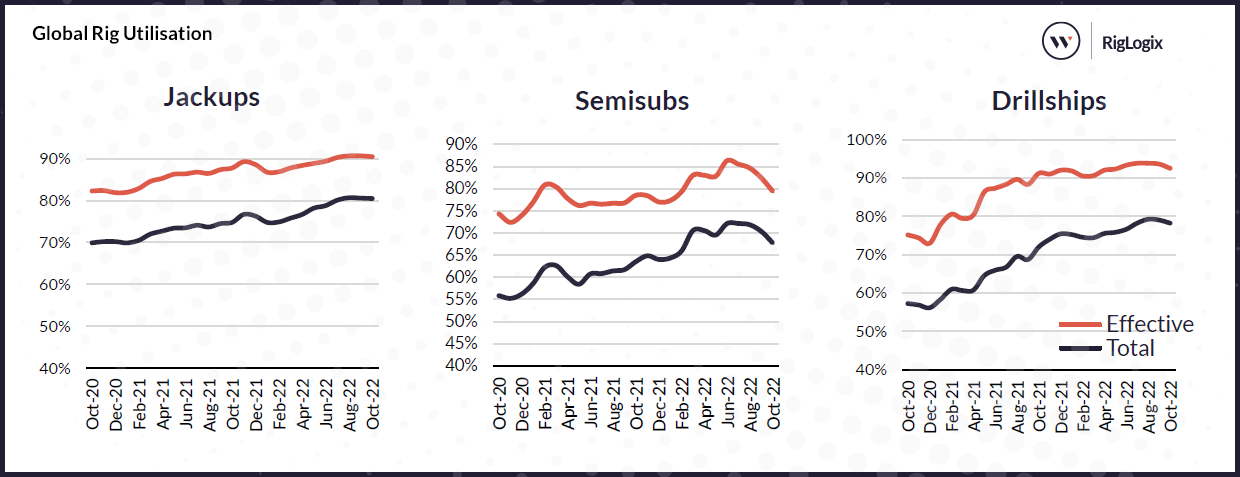

The global committed jackup count totalled 395 units in November, one rig higher than the previous month. The marketed available and cold stacked jackup counts now stand at 42 and 54, respectively. Marketed, committed utilisation and total fleet utilisation stayed at 91% and 81% for the month. There were 10 new fixtures and two options exercised during the month with a total of 12,580 drilling days. Saudi Aramco awarded 78% of the total drilling days with six five-year contracts, commencing in 2023.

The global committed semisubmersible (semi) count grew by one to 65 this month. There are 16 available rigs and 14 cold stacked units in the fleet. Marketed, committed utilisation rose to 80%, whilst total fleet utilisation maintained at 68%. There were six new fixtures and one option exercised with a total of 2,420 drilling days during the month. Most notably, Petrobras awarded a $429 million multi-year contract with Diamond Offshore for Ocean Courage to work off Brazil commencing in 4Q 2023.

Finally, drillship demand grew by one unit to 77 rigs after staying constant from September, leaving only four units available in the market, while another 15 rigs are cold stacked. Marketed, committed utilisation and total fleet utilisation raised to 95% and 80%, respectively. There were five new contracts and three options signed in November, totalling 2,175 drilling days. BP awarded Valaris DS-12 with a contract value of $136 million for Valaris DS-12 to work off Egypt in 2H 2023.

Offshore Field Development

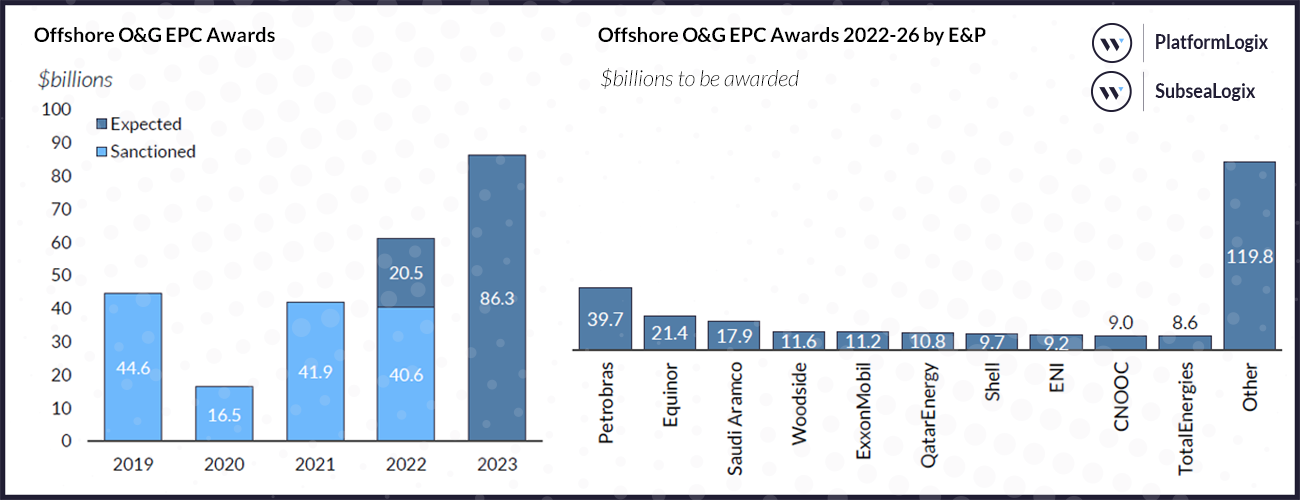

Offshore O&G-related engineering, procurement, and construction (EPC) contract award value in the last 30 days was estimated at US$4 billion, bringing the year-to-date total to US$40.6 billion (excluding letters of intent). EPC award value was predominantly driven by contract awards to Saipem for Saudi Aramco’s Abu Safah field and QatarEnergy’s North Field Compression Phase One project.

There has been a 32% downward revision in anticipated offshore EPC spend in 4Q 2022 compared to last month’s outlook, driven by Equinor’s decision to delay the final investment decision (FID) on its Wisting project until 2026. The operator stated that global inflation in the supply industry and uncertainty of execution capacity due to the war in Ukraine were the primary reasons for the delay. Furthermore, major EPC contract awards for QatarEnergy’s Ruya and the North Field South (NFS) developments have also been delayed due to the Qatar 2022 FIFA World Cup.

New Fortress Energy (NFE) awarded Sembcorp Marine a master service agreement for the engineering and conversion of two Sevan cylindrical drilling vessels to floating liquified natural gas (FLNG) units. The first unit is expected to be deployed on Pemex’s Lakach project, which the Mexican regulators recently approved following a revision to its development plan. This FLNG EPC award for the first unit has led to an increase in total FPS throughput capacity sanctioned in 2022 by approximately 12.5 kboepd.

Approximately US$20 billion in offshore EPC contract award value is forecast for the remainder of 2022, driven by Equinor and Aker BP’s investment offshore Norway for projects including the NOAKA development and the Skarv satellite projects. Looking into 2023, Westwood anticipates offshore O&G-related EPC spend to total US$86 billion, with the Americas accounting for 27%, whilst Africa and Western Europe will account for 14% and 8% respectively.

Offshore Wind

Since the last update, Siemens Gamesa signed two contracts for the three Hai Long wind farms, located offshore Taiwan. The first contract covers the supply of 73 SG 14-222 DD offshore wind turbines across the three projects and the second contract is a 15-year turbine service agreement with an option to extend this to 20 years. The 300 MW Hai Long 2a, 232 MW Hai Long 2b and 512 MW Hai Long 3 wind farms are being developed by a consortium of Yushan Energy, Northland Power, and Mitsui & Co.

Dominating headlines was news that the US Department of the Interior announced an offshore wind lease sale to be held on 6 December 2022 for areas on the Outer Continental Shelf (OCS) off central and northern California. The sale will be held by the Bureau of Ocean Energy Management (BOEM). A total of five lease areas with the potential to produce over 4.5 GW of offshore wind energy will be offered via a competitive auction.

Finally in the Netherlands, RWE Renewables was awarded the rights to develop the 760 MW Hollandse Kust West Site VII wind farm via a subsidy-free tender. The wind farm will be developed by RWE’s project company, Oranje Wind Power II. As part of the project plans, surplus electricity produced from the wind farm will be used to power green hydrogen production on land and floating solar panels will also be incorporated to use the ocean space more efficiently.

Offshore Drilling Rigs

| Contract Backlog Month-on-Month (Rig Years) | Jackups | Semisubs | Drillships |

| October 2022 | 743.3 | 90.5 | 131.9 |

| November 2022 | 724.7 | 91.4 | 130.8 |

| Difference | -18.6 | +0.9 | -1.1 |

*Correct as of 20th November 2022

The global committed jackup count totalled 394 units in October, two higher than the previous month. The marketed available and cold stacked jackup counts now stand at 41 and 54, respectively. Marketed, committed utilisation and total fleet utilisation stands at 91% and 81%. There were 21 new fixtures made during the month, with a total of 15,550 drilling days. More than 50% of these fixtures came from the Middle East, followed by 38% from the North America region.

The global committed semisubmersible (semi) count dropped by three to 64 this month. There are 17 available rigs and 14 cold stacked units in the fleet. Marketed, committed utilisation declined from 82% to 79%, while total fleet utilisation fell to 68%. There were five new fixtures with a total of 1,390 drilling days during the month. Most notably, Petrobras awarded LOIs for multi-year contracts to Ocyan (Norbe VI) and Diamond Offshore (Ocean Courage) to work off Brazil commencing in 3Q 2023.

Finally, drillship demand stayed constant from September at 76 units, leaving only six units available in the market, while another 15 rigs are cold stacked. Marketed, committed utilisation and total fleet utilisation dipped slightly to 93% and 78%, respectively. There were six new contracts signed in October, totalling 6,272 drilling days. Petrobras was responsible for five of the six awards, all LOIs for work commencing between 1Q and 3Q 2023 offshore Brazil.