Offshore Energy Data Dashboard

Each month Westwood’s Offshore and New Energies teams provide a global data update on oil and gas-related engineering, procurement and construction (EPC) awards, wind turbine generator (WTG) awards, and drilling rig fleet utilisation and contract backlogs for jackups, semi-submersibles and drillships. Offshore field development data is sourced from and analysed using PlatformLogix, offshore wind data is from WindLogix, and offshore drilling rig data is from RigLogix. Bookmark this page for regular updates on the health of the offshore energy and renewable sectors.

Offshore Field Development

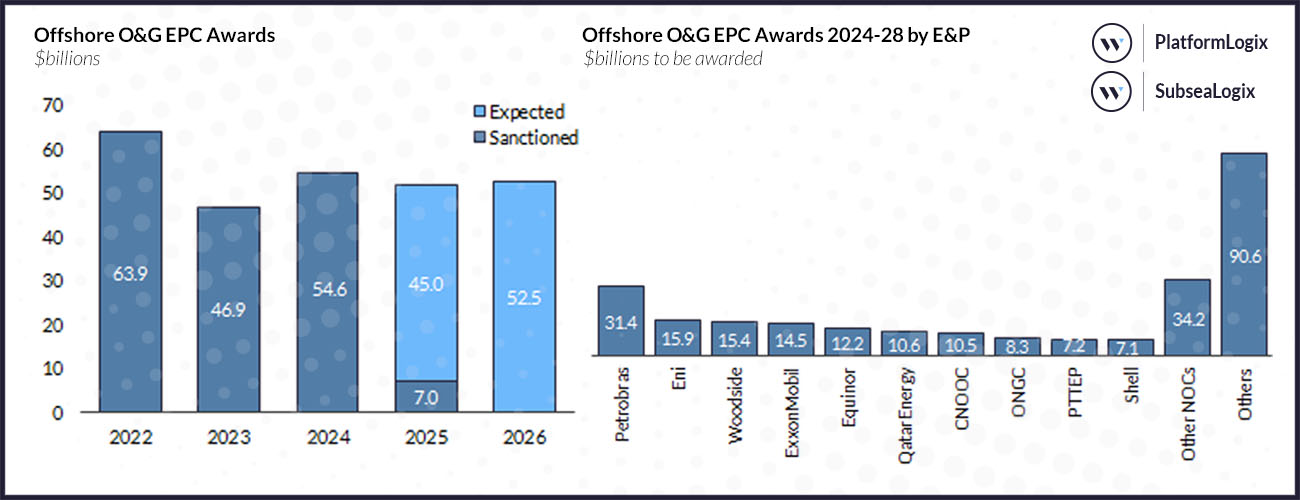

Offshore O&G-related engineering, procurement and construction (EPC) contract award value year-to-date is estimated at US$9bn (excluding letters of intent). Key highlights during the period under review include the announcement by BW Energy that it has taken a final investment decision (FID) on its Maromba field offshore Brazil, which will feature an integrated drilling and wellhead platform and a refurbished floating production storage and offloading (FPSO) unit, with first oil scheduled for late 2027. In the Gulf of Thailand, Valeura Energy sanctioned the redevelopment of its Wassana field, which involves the installation of a new central processing platform and associated export pipeline, with a total EPCC value of US$120mn. The initial drilling campaign comprises 16 horizontal development wells and one water injection well, with production expected to commence in 2Q 2027.

On 29 April, Subsea 7 announced the award of an EPCI work scope by BP to Subsea Integration Alliance (SIA) for the Ginger project offshore Trinidad and Tobago. Contracting activities that underpinned investment in May include the engineering, procurement, fabrication, installation, and pre-commissioning of 112km rigid risers and flowlines system work scope awarded to Subsea 7 for Petrobras’ Buzios XI development offshore Brazil. Subsea 7 also announced an award for the transportation and installation (T&I) of flexible pipelines, umbilicals and subsea components for an undisclosed project offshore West Africa.

For the remainder of 2025, Westwood forecasts offshore O&G-related EPC contract award value to total US$43bn, underpinned by c.240 subsea tree units, 12 floating production platforms and 70 fixed platform units.

Offshore Wind

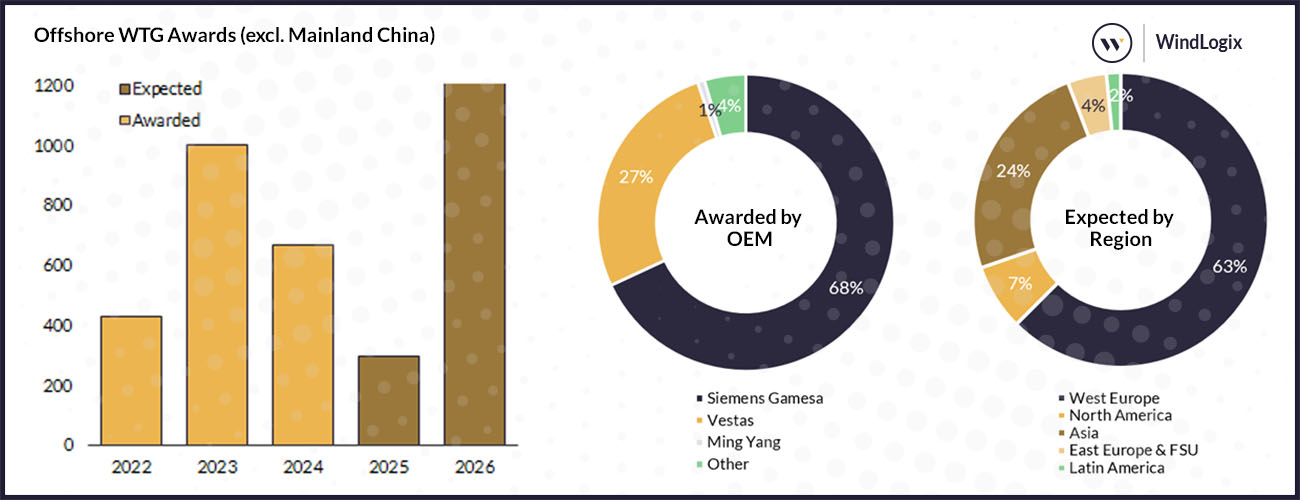

Since the last update no turbine supply contracts have been awarded, however Google signed its first offshore wind power purchase agreement (PPA) in Taiwan, and in the broader Asia Pacific region, with Copenhagen Infrastructure Partners (CIP). The deal covers electricity from the 495MW Fengmiao Phase I offshore wind farm, which reached financial close in March 2025.

Dominating headlines was news that Orsted is halting the development of the 2.4GW Hornsea Project Four wind farm located offshore England, UK. The developer stated that this decision has been made due to increases in supply chain costs, higher interest rates, and an increase in the risk to construct and operate the wind farm within the planned time frame. Orsted also stated that it will evaluate options for future development of the wind farm given its continuing seabed rights, grid connection agreement and Development Consent Order.

Finally, The Norwegian government has launched the Utsira Nord floating offshore wind lease tender round. The deadline for applications is 15 September 2025. The allocation of lease sites and state aid will take place in two stages. In the first stage, three project areas will be allocated to the bidders who score the highest in a competition based qualitative criteria. State aid will be awarded through a competitive process following a maturation phase. To participate, developers must submit a license application and a bank guarantee. The auction will proceed only if at least two qualified developers apply.

Offshore Drilling Rigs

| Contract Backlog Month-on-Month (Rig Years) | Jackups | Semisubs | Drillships |

| April 2025 | 867.4 | 82.0 | 157.8 |

| May 2025 | 838.6 | 77.3 | 152.6 |

| Difference | -28.7 | -4.7 | -5.2 |

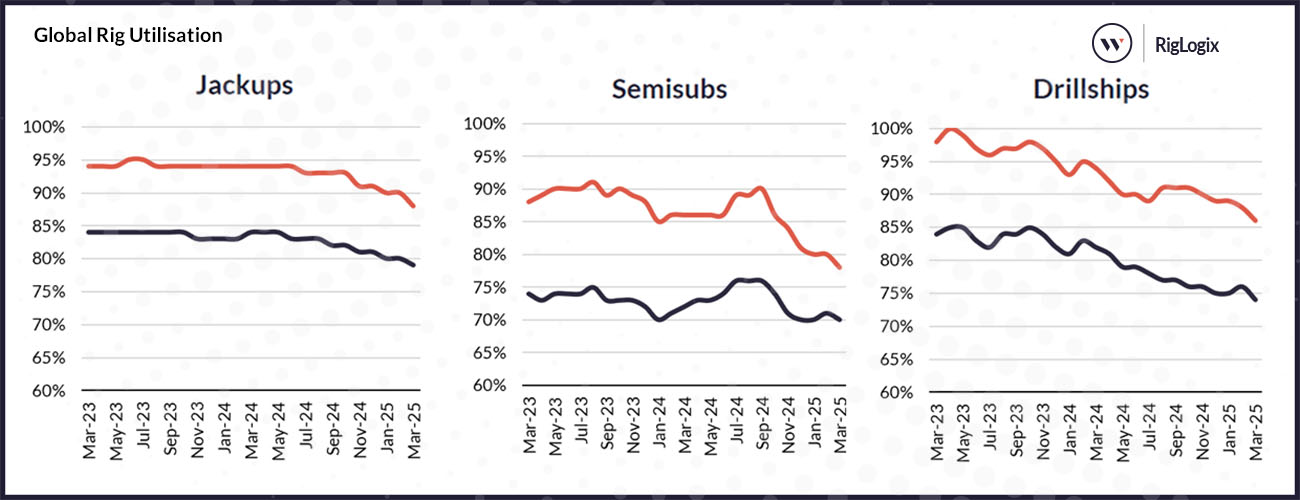

The global committed jackup fleet remained at 391 units in April. Marketed available and cold-stacked jackup counts now stand at 52 and 54 respectively, with marketed committed utilisation and total utilisation at 88% and 79% respectively. During the month, a total of 17 new contracts were awarded, amounting to 16,175 days (44.3 rig years) of backlog added. Advanced Energy Systems (ADES) Admarine V was awarded a 1095-day contract by Petrobel to drill offshore Egypt in April 2025, at an undisclosed dayrate.

The global committed semisubmersible count increased by one to 60 units in April, with 16 available and eight cold-stacked rigs remaining in the fleet. During the month, marketed committed and total utilisation increased to 79% and 71% respectively. There were three recorded fixtures, amounting to 482 days (1.3 rig years) of backlog added. Transocean Equinox had its two 45-day options exercised by Zenith Energy to drill offshore Australia in June 2026, at a dayrate of $540,000.

Finally, the global committed drillship count increased by three to 78 units during the month, leaving 11 marketed rigs available plus 13 cold-stacked units. Marketed committed and total utilisation increased to 88% and 76% respectively. Seven new fixtures were recorded in March. Noble Globetrotter I was awarded a 45-day contract by Murphy oil to drill offshore US in April 2025, at a dayrate of $350,000. Noble Venturer was awarded a 16 well, 1060-day contract by Total Energies to drill offshore Suriname in October 2027, at an undisclosed dayrate.

Offshore Field Development

Offshore O&G-related engineering, procurement and construction (EPC) contract award value year-to-date is estimated at US$7bn (excluding letters of intent). During the period under review, Eni confirmed it had reached financial close with the UK government at the Liverpool Bay carbon capture and storage (CCS) project, and has moved into the construction phase, which involves the repurposing of part of offshore platforms, 149km of onshore and offshore pipelines, and the construction of a new 35km pipeline.

A key CCS contract recorded during the period under review is for the Northern Lights Carbon Storage phase II project, for which Subsea 7 was awarded the EPCI contract for a 5km pipeline, whilst OneSubsea is expected to supply the subsea trees required for the project.

In April 2025, ExxonMobil issued a Limited Notice to Proceed (LNTP) to Saipem for the EPCI work scope for the subsea umbilicals, risers and flowlines (SURF) for its Hammerhead project in the Stabroek block offshore Guyana. Modec also confirmed an LNTP for the floating production, storage and offloading (FPSO), which allows the contractor to proceed with the front-end engineering and design (FEED) work scope of the contract, whilst confirmation of the EPCI work scope is pending on governmental and regulatory approval, which Westwood anticipates will be granted before the end of 2Q 2025.

Year-to-date, Westwood has recorded 39 subsea tree units awarded, three floating production units and 19 fixed platforms. For the remainder of 2025, Westwood forecasts offshore O&G-related EPC contract award value to total c.US$45bn.

Offshore Wind

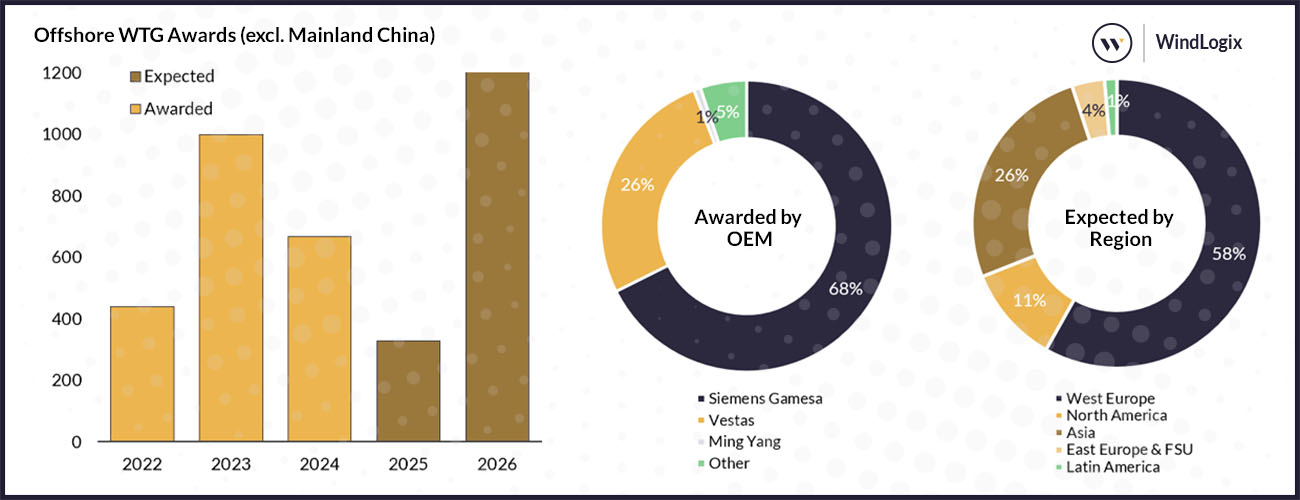

Since the last update, Vestas has been awarded contracts to supply its V236-15.0 MW turbines at two wind farms. A total of 33 turbines have been ordered for the Fengmiao I wind farm in Taiwan and the contract includes a long-term comprehensive service agreement. Vestas has also been awarded a firm contract to supply a total of 68 turbines at the Nordlicht I wind farm, located offshore Germany. The scope of the contract includes a five-year service and warranty agreement followed by a 25-year operational support agreement.

Dominating headlines was news that the EFTA (European Free Trade Association) Surveillance Authority (ESA) has approved the support system proposed by the Norwegian government for the upcoming Utsira Nord projects. NOK35bn (US$3.3bn) is being made available by the Norwegian government, with an auction expected in 2028/29, allowing time for the maturation of projects soon to be awarded in the Utsira Nord lease auction.

Finally, the final phase of the UK’s Celtic Sea floating wind leasing round has begun. The first phase, which required participants to submit project proposals alongside plans for working with ports and creating socio-economic benefits, has been completed. Evaluation of these proposals has now concluded, and successful bidders have been invited to progress to the final stage. This will involve an auction in which final bids will be submitted. The auction is expected to take place in June 2025 and winning bidders are then expected to sign Agreements for Lease in late summer 2025.

Offshore Drilling Rigs

| Contract Backlog Month-on-Month (Rig Years) | Jackups | Semisubs | Drillships |

| March 2025 | 832.2 | 83.2 | 151.8 |

| April 2025 | 816.3 | 79.0 | 146.0 |

| Difference | -15.9 | -4.2 | -5.8 |

The global committed jackup count decreased by four to 391 units in March. Marketed available and cold-stacked jackup counts now stand at 53 and 53 respectively, with marketed committed utilisation and total utilisation at 88% and 79% respectively. During the month, a total of 15 new contracts were awarded, amounting to 4,367 days (12 rig years) of backlog added. Velesto Energy Naga 2 was awarded a 120-day contract by Northern Gulf Petroleum to drill offshore Thailand in May 2025, at a dayrate of $93,000.

The global committed semisubmersible count decreased by two to 59 units in March, with 17 available and 8 cold-stacked rigs remaining in the fleet. During the month, marketed committed dropped to 78%, while total utilisation remained at 70%. There was only one fixture, where Island Drilling’s Island Innovator was awarded a 1096-day contract by Equinor ASA to drill offshore Norway in January 2026, at a dayrate of $300,000.

Finally, the global committed drillship count decreased to 75 units during the month, leaving 13 marketed rigs available plus 14 cold-stacked units. Marketed committed and total utilisation decreased to 86% and 74% respectively. Seven new fixtures were recorded in March. Valaris DS-10 was awarded a 730-day contract by an undisclosed operator, who is believed to be Shell, to drill offshore Nigeria in June 2026 at a dayrate of $482,000. Noble Viking was awarded a 30-day contract by Brunei Shell to drill offshore Brunei Darussalam in November 2025, at a dayrate of $466,666.

Offshore Field Development

Offshore O&G-related engineering, procurement and construction (EPC) contract award value year-to-date is estimated at US$2.4bn (excluding letters of intent). During the period under review, ExxonMobil sanctioned the development of its Turrum phase III project offshore Australia. However, PTTEP cancelled the EPC tender for its Lang Lebah project offshore Malaysia, stating that commercial tenders were significantly above its project budget. This and Petrobras’ decision to cancel the tender for its Barracuda/Caratinga floating production, storage and offloading (FPSO) tender contributed to a 12% downward revision in Westwood’s 2025 EPC award value compared to last month’s outlook, as E&Ps continue to evaluate project economics in the face of supply chain inflationary pressures and macro headwinds in 2025. It is pertinent to state that no subsea tree contract nor FPSO contracts were announced during the period under review.

Over the last 30 days, several subcontracts were confirmed, including the award by McDermott to Chiwan Sembawang Engineering (CSE) for the construction of a 9000-tonne jacket for a processing platform to be installed at the North Oil Company’s (NOC) Ruya development offshore Qatar. EnerMech was awarded a pre-commissioning work scope by SBM Offshore for its One Guyana FPSO to be installed on ExxonMobil’s Yellowtail project offshore Guyana, whilst TMC Compressors was awarded a contract to supply its high-capacity marine compressed air system for the floating liquefied natural gas (FLNG) unit destined for Genting Oil & Gas’s AKM development, Indonesia.

For the remainder of 2025, Westwood forecasts offshore O&G-related EPC contract award value to total c.US$46bn, underpinned by c.240 subsea tree units, 12 floating production units (including four FLNG units), 90 fixed platforms, 3,400km of SURF and 2,450km of line pipes.

Offshore Wind

Since the last update no turbine supply contracts have been awarded, however Siemens Gamesa announced that it will expand its turbine blade manufacturing facility in Le Harve, France. The company will invest EUR200mn (US$209mn) on the expansion and it will allow them to produce 115m long turbine blades for its 14MW turbines. Construction on the expansion is scheduled to be completed in 2026.

In terms of policy news, the UK government launched a consultation on proposed reforms to the Contracts for Difference (CfD) Allocation Round 7 (AR7) subsidy auction. Proposed changes include:

- A relaxation of CfD eligibility criteria for fixed-bottom offshore wind projects to permit projects that have not yet obtained full planning consent to participate, allowing CfDs to be awarded at an earlier stage of the project lifecycle.

- Increasing the length of the CfD contract from the current 15-year term.

- Amending the budget publication process and information received by removing the requirement to publish a Contract Budget Notice at the opening of the allocation round for all technologies and instead to publish the Contract Budget Notice after the allocation round has run.

Finally, the Offshore Wind Power Special Act, which mandates the transition of offshore wind power development to a government-led planned site system, has passed the South Korean National Assembly plenary session. With bipartisan support securing its final legislative approval, it now awaits the president’s endorsement following a Cabinet meeting.

Offshore Drilling Rigs

| Contract Backlog Month-on-Month (Rig Years) | Jackups | Semisubs | Drillships |

| February 2025 | 845 | 83.7 | 154.2 |

| March 2025 | 817.2 | 80.0 | 148.4 |

| Difference | -27.7 | -3.7 | -5.8 |

*Correct as of 10th March 2025

The global committed jackup count decreased by two to 395 units in February. Marketed available and cold-stacked jackup counts now stand at 48 and 54 respectively, with marketed committed utilisation and total utilisation at 89% and 79% respectively. During the month, a total of 12 new contracts were awarded, amounting to 3,989 days (10.9 rig years) of backlog added. TotalEnergies exercised its 600-day option for the Valaris Stavanger to continue drilling in the UK North Sea from July 2025 through March 2027, at a dayrate of $125,000.

The global committed semisubmersible count decreased by one to 61 units in February, with 15 available and 11 cold-stacked rigs remaining in the fleet. During the month, marketed committed utilisation remained at 80%, while total utilisation remained at 70%. Burullus Gas exercised its 160-day option for Saipem’s Scarabeo 9 to drill two wells from April 2025.

Finally, the global committed drillship count decreased to 77 units during the month, leaving 11 marketed rigs available plus 14 cold-stacked units. Marketed utilisation increased to 88%, while total utilisation increased to 76%. Three new fixtures were recorded in February. Seadrill’s West Vela was awarded a 40-day contract by Talos Energy to drill offshore the U.S. in August 2025, at a dayrate of $490,000.

Offshore Field Development

Offshore O&G-related engineering, procurement and construction (EPC) contract award value in January 2025 was estimated at US$1.8bn (excluding letters of intent). During the period under review, Petronas announced it had reached a final investment decision (FID) for the development of its Hidayah field located in the North Madura II Contract Area, East Java, offshore Indonesia. DIALOG Resources also announced FID for its Baram Junior Cluster Small Field Asset Production Sharing Contract, amounting to US$235mn. However, there was disappointment on the FID front, as Santos opted not to proceed with the planned FID for the Dorado project offshore Australia, which meant it decided not to acquire the identified floating production, storage and offloading (FPSO) unit and commence front-end engineering and design (FEED) studies on the project.

In January, Equinor awarded a parallel early engineering contract to both Altera Infrastructure and BW Offshore for a FPSO unit to be deployed at its Bay du Nord project offshore Canada. Other major FEED contracts awarded during the period include Subsea 7’s SURF work scope for Equinor’s Fram Sor, which included an EPCI option. ICE Marine Design Group was also awarded a fast-track FEED work scope relating to the hull engineering of the Aoka Mizu FPSO unit to be installed at Navitas Petroleum’s Sea Lion field offshore the Falkland Islands.

For the remainder of 2025, Westwood forecasts offshore O&G-related EPC contract award value total US$53bn, underpinned by c.290 subsea tree units, 14 floating production units (including four FLNG units), 90 fixed platforms, ~4,000km of SURF and ~2,460km of line pipes.

Offshore Wind

Since the last update no turbine supply contracts have been awarded, however the developers of the 1,080 MW Inch Cape wind farm announced that they reached financial close, raising more than £3.5bn (US$4.4bn) of funding. Terms for the project financing have been reached with lenders comprising of 22 commercial banks.

Orsted and PGE announced that they have taken a FID on the 1,498 MW Baltica 2 wind farm, located offshore Poland. The wind farm will feature a total of 107 SG 14-222 DD turbines that will be supplied by Siemens Gamesa, and it is scheduled to come online in 2027.

An Executive Order has been issued by the new US President, pausing offshore wind leasing, as well as permitting for both offshore and onshore wind. Under the order, the President has withdrawn “from disposition for wind energy leasing all areas within the Offshore Continental Shelf (OCS).” With regards to permitting the order states that no agency is allowed to “issue new or renewed approvals, rights of way, permits, leases, or loans for onshore or offshore wind projects pending the completion of a comprehensive assessment and review of Federal wind leasing and permitting practices.”

Finally, the tender for the rights to develop the 1 GW Project Site N-9.4, located offshore Germany, was launched. A maximum bidding price of EUR0.62 cents/kWh (US$0.64/kWh) has been set. The deadline for the submission of bids is 1 June 2025 and the wind farm is scheduled to come online in 2032.

Offshore Drilling Rigs

| Contract Backlog Month-on-Month (Rig Years) | Jackups | Semisubs | Drillships |

| January 2025 | 863.1 | 85.1 | 157.0 |

| February 2025 | 832.0 | 80.6 | 151.2 |

| Difference | -31.1 | -4.5 | -5.8 |

*Correct as of 10th February 2025

The global committed jackup count decreased by five to 397 units in January. Marketed available and cold-stacked jackup counts now stand at 46 and 57 respectively, with marketed committed utilisation and total utilisation at 90% and 80%, respectively. During the month, a total of four new contracts were awarded, amounting to 587 days (1.6 rig years) of backlog added. The Admarine 504 has been awarded a 365-day contract by Britannia U to drill six wells from March 2025.

The global committed semisubmersible count remained at 62, with 14 available and 12 cold-stacked rigs remaining in the fleet. During the month, marketed committed utilisation increased to 81%, while total utilisation remained at 70%, respectively. The Deepsea Atlantic has been awarded a 331-day contract by Equinor ASA to drill offshore Norway from August 2026 through June 2027, at a dayrate of $450,000.

Finally, the global committed drillship count increased to 79 units during the month, leaving 12 marketed rigs available plus 14 cold-stacked units. Marketed utilisation increased to 87% while total utilisation remained at 75%, respectively. Three new fixtures were recorded in January. Stena DrillMAX has been awarded a 45-day contract by TotalEnergies to drill one well in May 2025. Additionally, Eni exercised its two 60-day contract options on Saipem 10000, keeping the rig busy through to May 2025.

Offshore Field Development

Offshore O&G-related EPC contract award in 2024 is estimated to have closed at US$52bn (excluding letters of intent), underpinned by over 250 subsea tree units, 11 floating production units (including three FLNG units), over 66 fixed platforms, ~2,800km of SURF and ~1,900km of line pipes.

Contract awards recorded in December 2024 were underpinned by major FID announcements, such as Shell’s Bonga North development offshore Nigeria, where TechnipFMC was awarded the contract to design and manufacture subsea tree systems, manifolds, jumpers, controls and services for up to 16 wells required for the development. Saipem was awarded the EPCI work scope for the SURF and subsea structures, valued at US$900mn, with support from its Nigerian partners Koa Oil & Gas and Aveon Offshore. Other FID announcements in December include Shell’s Silvertip Ph.3 development and Beacon Offshore’s Zephyrus oil discovery and the Shenandoah Ph.2 development, all in the US GoM. Following FID for the Northern Endurance partnership’s CCS project in the UK North Sea, TechnipFMC confirmed the iEPCI contract award for the CCS project that covers the supply and installation of an all-electric subsea system, with Saipem confirming the EPCI work scope for a 143km, 28-inch offshore CO2 pipeline for the CCS project.

Looking ahead to 2025, Westwood forecasts offshore O&G-related EPC contract award value to experience a marginal 1% YoY increase, totalling US$54bn, underpinned by 53 greenfield and brownfield field FIDs. EPC contracting activities in 2025 are to be driven by the demand for over 290 subsea tree units, 18 floating production units (including four FLNG units), over 90 fixed platforms, ~3,650km of SURF and ~2,660km of line pipes.

Offshore Wind

Since the last update Vestas signed a firm contract for the supply, installation and commissioning of 72 V236-15.0 MW turbines at the 1,080 MW Inch Cape wind farm located offshore Scotland, UK. The contract also includes a 10-year service agreement, followed by an operational support agreement. Vestas also received a firm order to supply turbines for the 315 MW Akita-Katagami-Oga wind farm, located offshore Japan. Vestas will supply a total of 21 V236-15.0 MW turbines and this contract also includes a long-term service agreement.

Dominating headlines was news that BP and JERA have agreed to form an offshore wind JV company. The JV will be equally owned, and it is expected to focus on progressing existing projects in northwest Europe, Australia and Japan and to continue to mature the development pipeline of significant longer-term opportunities. Up to US$5.8bn in capital funding for investments will be committed by the two partners by the end of 2030 to support this plan.

Finally, Japan announced the award of two lease sites (Yuza and Aomori South). The 450 MW fixed-bottom Yuza site has been awarded to BP and its partners, Marubeni, Kansai Electric Power, Tokyo Gas and Marutaka Corporation. The site is anticipated to feature 30 of Siemens Gamesa’s 15 MW turbines. The 615 MW Aomori South site has been awarded to a consortium comprising JERA, Green Power Investment and Tohoku Electric Power. The project is also anticipated to utilise Siemens Gamesa’s 15 MW turbines.

Offshore Drilling Rigs

| Contract Backlog Month-on-Month (Rig Years) | Jackups | Semisubs | Drillships |

| December 2024 | 895.2 | 87.7 | 162.9 |

| January 2025 | 872.3 | 85.1 | 157.4 |

| Difference | -22.9 | -2.6 | -5.5 |

*Correct as of 10th January 2025

The global committed jackup count decreased by three to 402 units in December. Marketed available and cold-stacked jackup counts now stand at 41 and 57 respectively, with marketed committed utilisation and total utilisation at 91% and 81%, respectively. During the month, a total of 26 new contracts were awarded, amounting to 24,736 days (67.8 rig years) of backlog added. 12,045 days were extensions of evergreen contracts for 11 rigs operated by CNOOC. Additionally, 7,304 days were awarded to Dana and Al Jurf for drilling operations in the UAE by ADNOC Offshore. PTTEP awarded ADES’ Admarine 503, a suspended rig previously operated by Saudi Aramco, a five-year firm contract for work in the Gulf of Thailand from October 2025 to September 2030.

The global committed semisubmersible count decreased by one to 62, with 15 available and 11 cold-stacked rigs remaining in the fleet. During the month, marketed committed and total utilisation dropped to 80% and 70%, respectively. The Noble Developer has been awarded a 200-day contract by Petronas to drill three wells from June 2025 through December 2026, at a dayrate of $400,000.

Finally, the global drillship count dropped to 77 units during the month, leaving 13 marketed rigs available plus 13 cold-stacked units. Marketed utilisation and total utilisation dropped to 86% and 75%, respectively. Twelve new fixtures were recorded in December. The Noble Venturer has been awarded a 120-day contract by Tullow Oil to drill two wells from May 2025 through August 2025, at a day rate of $460,000.

Mark Adeosun, Offshore Director

PlatformLogix & SubseaLogix

Bahzad Ayoub, Senior Analyst

WindLogix

Terrence Teo, Junior Rig Analyst

RigLogix