Completion efficiencies in the Marcellus/Utica formations of the US Northeast have changed the perception of the mature gas basin. The implementation of longer laterals and increased proppant loading intensity have lowered production costs and raised production. However, pressure pumpers in the Appalachia are expecting a slow-down in the back half of 2018 due to operators reaching production targets sooner than expected given increased operational efficiencies.

Recent data shows a 9% decline in Marcellus fleet utilization. In June, utilization totaled approximately 93% in the basin. This amount reduced to 85% in July. Furthermore, the Marcellus completion market wasn’t aided by a ramp-up in fleet sizes between 1Q18 and 2Q18, as pressure pumpers were making sure they could match operator demand.

Market Share: Top Priority

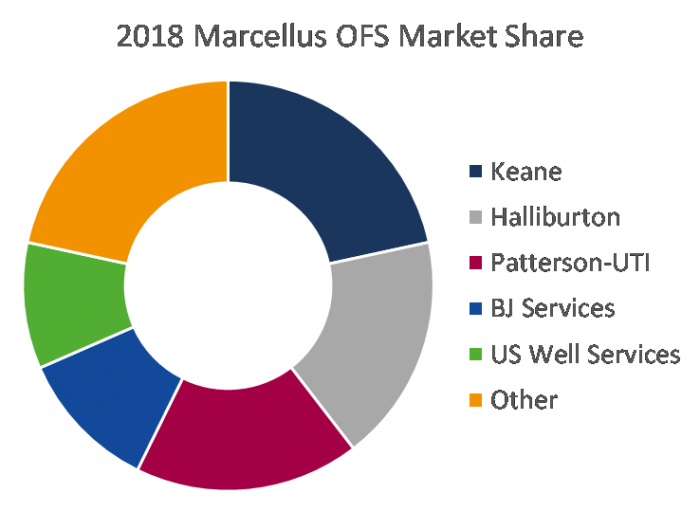

Given what pressure pumpers are deeming to be a short-term set back, OFS companies are not willing to sacrifice market share to accommodate pricing (Figure 1).

Figure 1. Marcellus Pressure Pumping Market Share in 2018 YTD Source: Energent Group

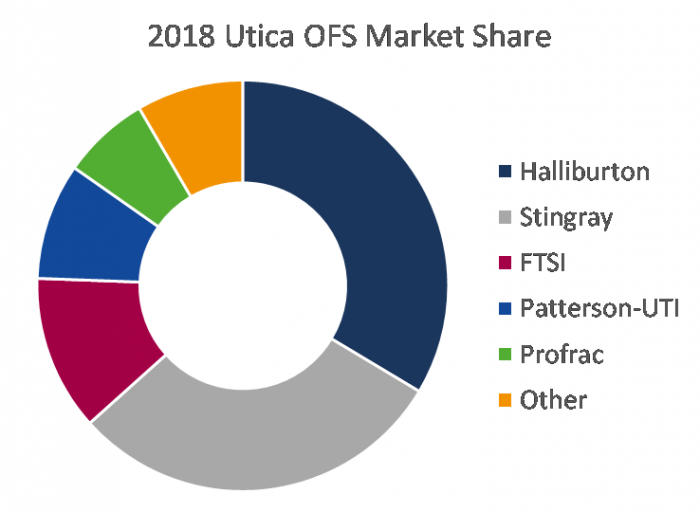

Halliburton is one of the leading pressure pumpers in the US Northeast, with the second largest market share in the Marcellus YTD and the largest in the Utica, at 34%. The oilfield services giant said it is a “victim of [its] own success,” as longer laterals and better production has reduced the demand for its frac fleets. As a result, Halliburton is expecting pricing constraints in the third quarter. The OFS giant said it will wait out the slowdown rather than taking action to its improve margins and risk weakening its long-term position.

Although Halliburton admits to hearing “talks” of a back half 2018 slowdown, Marcellus OFS market share leader Keane says it has yet to see any impact on its utilization rates and expects them to hold steady through the year’s end. The company has 35% of its fleet running across the entire US Northeast. The company deployed the first of three newbuild fleets in June within the basin.

Source: Energent Group

Patterson-UTI (Universal Pressure Pumping) maintains a strong position in both the Marcellus and Utica shale plays. Recent reports from the company indicate that Patterson feels the Marcellus and other basins are oversupplied with horsepower. Approximately 31% of Patterson’s horsepower resides in the Marcellus and Utica.

BJ Services has 15% of the company’s total horsepower exposed to the Marcellus. The 5 frac crews in the Marcellus and Utica regions are at 100% utilization.

Meanwhile, FTS International has already been impacted in the Marcellus, with one of its largest customers cutting fleets. FTSI believes it will put some of the fleets back on the market in 2019 but admitted it’s still “too early to say that.”